Episode 5: Running on Empty - The Russian Endgame Is Here to Stay

What happens inside Russia won't stay inside Russia

Executive Summary

Russia’s fuel crisis has entered a new phase. What began as a logistics problem has become a volume problem. According to our analysis, refinery throughput has fallen from roughly 5.0mbpd in 2022 to just 2.9mbpd in early July 2026, leaving the country unable to meet domestic demand across gasoline, diesel and other refined products.

Gasoline shortages are now nationwide, diesel has followed, exports have collapsed and are now banned, rationing has spread across most federal subjects, and the Kremlin has quietly shifted from denial to damage control.

Ukraine’s drone campaign is no longer simply destroying refineries. It is steadily degrading Russia’s ability to convert crude oil into usable fuel, bringing the war home to Moscow and, finally, to ordinary Russians.

The obvious solution, imports, turns out to be far less obvious in practice. Russia must simultaneously overcome sanctions, economics, logistics, shipping and, increasingly, maritime security constraints to replace lost domestic production. Belarus and India can provide partial relief. China is unlikely to come to the rescue. None can close the gap at scale. Imports can cushion the shortages. They cannot eliminate them.

The implications extend far beyond empty filling stations. Fuel is the bloodstream of a modern economy, and in a country spanning eleven time zones every missing barrel ripples through trucking, agriculture, food prices, freight markets, inflation, shipping, military logistics and, ultimately, political stability.

This report is therefore not simply about Russian gasoline shortages. It is about identifying the second- and third-order consequences of a structural deterioration in Russia’s fuel balance and how that is reshaping global trade flows, refining margins, freight markets and capital allocation. The chapter What’s the Trade? explores those implications in detail.

This report follows my earlier Substack from October 2025, Running on Fumes: How Refinery Strikes and Urals Economics Threaten Russia’s Oil Output – and Its Regime. I recommend reading it first if you want the broader strategic context (paywall).

Finally, I will keep this report free until the Investment Section. I have spent more than twenty years investing in commodities and believe deeply that capital markets ultimately rest on something far more important than markets themselves: freedom, private property and the rule of law. Those are precisely the values Ukraine is defending today. If this research helps journalists, OSINT researchers, policymakers, investors or simply those trying to separate fact from propaganda better understand what is happening inside Russia’s refining system, then making it public is worthwhile.

If you find it useful, please share it. Reliable, timely data on Russia’s fuel system are expensive to obtain, painstaking to verify and increasingly difficult to assemble. I hope this report makes a small contribution to understanding how the refinery campaign is reshaping Russia’s economy, military logistics and, ultimately, its ability to wage this war.

Enjoy.

Alexander

Unpopular Methods

Black smoke rose over Omsk on the morning of 6 July. The Gazprom Neft refinery there is Russia’s largest, 2,500 kilometres from Ukraine, deep in Western Siberia, and until that morning the last great gasoline plant Kyiv had barely touched. It was simply out of reach. Not any more.

By nightfall, NASA satellites were detecting fires across the site. A thousand miles to the west, drivers queued at the few Moscow filling stations still selling fuel; in Crimea, a litre had climbed to a price that one resident said “soon there’ll be nothing left to compare it to.” The country that calls itself an energy superpower can no longer keep its own pumps flowing.

You do not have to take the President of Ukraine’s word for how bad it has become. Take the Kremlin’s.

That same day, Vladimir Solovyov, the Kremlin’s wannabe Goebbels, who has spent four years insisting night after night on Russia’s main state television channel that everything was under control and victory inevitable, finally admitted reality. The shortages are real. Deputy Prime Minister Alexander Novak’s assurance that there is “enough fuel” is a lie. “Everyone,” he conceded, “understands the real situation.”

For once, the propagandist and the petrol queue agreed.

Then he showed us how the Kremlin thinks: “War is not about popularity,” he declared. “It is about victory.” In the very next breath he warned his own people that “unpopular methods” were coming.

That single sentence is the key to the entire regime.

They lied while the lie still worked. The moment it stopped working, the moment ordinary Russians began complaining publicly at filling stations across roughly seventy-eight of Russia’s eighty-three federal subjects, the state reverted to its oldest instinct. It turned on its own people. It blamed the oil barons. “You found the money to buy footballers, but not a kopeck to defend your refineries. Who are you working for?” Revolutionary rhetoric from 1917 suddenly returned to Russian television. The promise of the truncheon followed shortly afterwards.

Which tells you what this really is. This stopped being an energy story some time ago. It is now a regime-survival story. The drones burning Russia’s refineries have done more than ration petrol. They have stripped the paint off the Kremlin’s machinery and exposed the fear beneath it.

Fuel is the bloodstream of a continental economy. Once it stops flowing, everything else follows: logistics, food prices, inflation, industrial production, public confidence and, ultimately, political stability. What follows is the anatomy of that fear: where the fuel actually goes, why the Kremlin cannot put the fire out, and why a state that insists it is winning is quietly preparing for the only war it truly fears: the one at home.

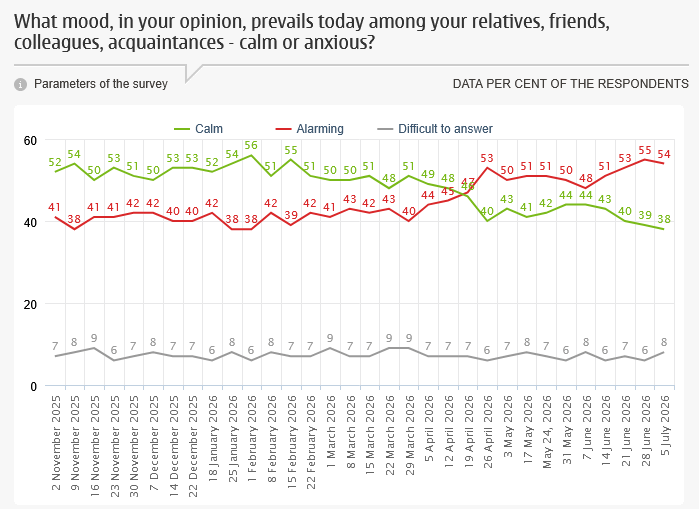

Listen to it yourself. I believe this is the single most important clip to emerge from Russia since the full-scale invasion of Ukraine began in February 2022, back when it was still called a “special military operation” and supposedly measured in days. Today Russia is running short of something far harder to replace than missiles: men. Ukraine is reportedly inflicting casualties faster than Russia can replenish them, roughly 35,000 killed or wounded every month. Sooner or later, the Kremlin will have to reach for the most unpopular measure of all: general mobilisation. That, too, is what Solovyov means when he speaks of “unpopular methods”.

Not since reservists were first mobilised in September 2022 have Russians felt so uneasy. On 2 July, the Public Opinion Foundation (FOM), a pollster closely aligned with the Kremlin, reported that 55% of respondents believed their relatives and colleagues felt anxious, up from 40% a year earlier. Russia’s post-Soviet social contract, whereby citizens stayed out of politics and the authorities largely left them alone, has broken down. The war has come home and become everybody’s problem. Drone attacks, once confined to border regions such as Kursk and Belgorod, now reach deep into the Russian interior. On 6 July, Ukrainian drones struck Russia’s largest refinery in Omsk, some 2,500 kilometres from the front line.

Petrol is now being rationed across much of Russia. Drivers queue for hours to purchase no more than 20 or 30 litres before being turned away, while many filling stations have simply run dry. According to T-Bank, which analyses millions of anonymised card transactions in real time, roughly one-quarter of Russian filling stations sold less fuel in June 2026 than a year earlier, despite transaction volumes remaining broadly unchanged. That is exactly what genuine physical shortages look like.

Meanwhile, the Kremlin’s preferred explanation is “panic buying”. To be sure, once shortages emerge, panic buying amplifies them. That is a feature of virtually every supply crisis. It is not the cause. The shortages themselves are real and reflect a structural deterioration in Russia’s fuel balance, as the data throughout this report will demonstrate.

The consequences are already rippling through the wider economy. Logistics companies are struggling to secure fuel. Disruptions to food deliveries are becoming increasingly likely. Food inflation is worsening, with potato prices rising 4.5% in June alone. Some farmers have already warned that they may be unable to harvest their crops if the shortages persist.

A refinery war has become an economic war. Economic wars are not measured by explosions or satellite imagery. They are measured by inflation, empty shelves, disrupted supply chains and collapsing public confidence. Those are ultimately the metrics that determine how long governments survive.

The Shortages

Mikhail Khodorkovsky, the man who once ran Yukos, Russia’s largest oil company, and whose former Samara refineries are now among those now burning, puts his finger on an important part of the story in a recent post on X [link]. By volume, he argues, this is not yet a catastrophe.

The breakdown, he continues, lies less in the barrels than in the brain: logistics and decision-making. Moving fuel across eleven time zones requires pipelines, rail tankers, strategic reserves and, above all, a state capable of deciding quickly what goes where. That state no longer exists. The people who once knew how to run it have emigrated, been sidelined or simply refuse to touch it. That, he argues, explains why shortages have spread to Chita and Irkutsk, thousands of kilometres from any front line.

Logistics are undoubtedly an issue. Decision-making is too. But they are no longer the binding constraint. Volumes are.

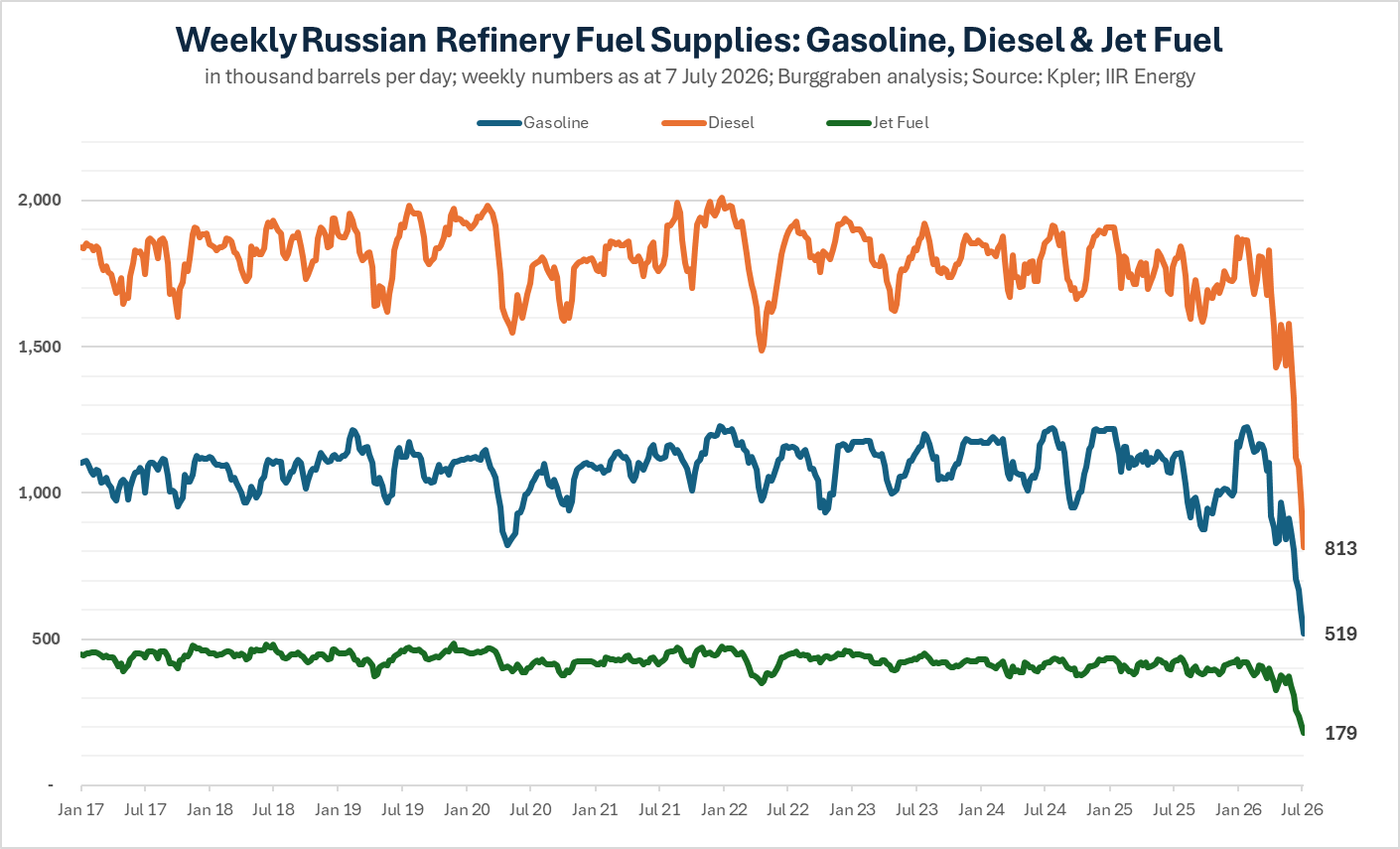

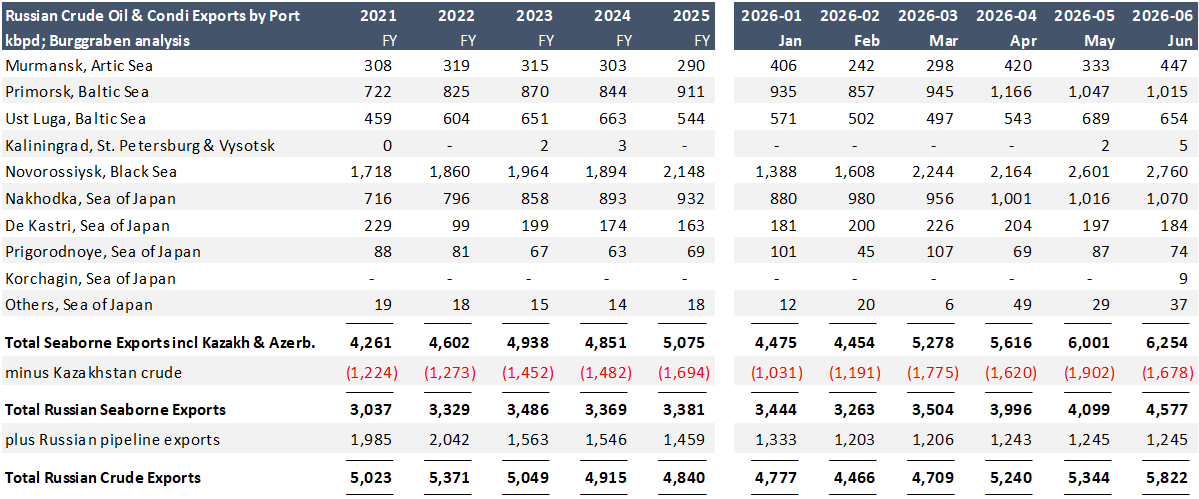

According to our data, Russian refinery throughput has fallen to just 2.9mbpd, down from our 2022 baseline of 5.0mbpd. At those levels, petroleum-product exports are effectively off the table, replaced instead by higher crude exports as Russia ships abroad the barrels it can no longer refine at home.

Against domestic petroleum-product demand of roughly 3.2mbpd, encompassing gasoline, diesel, jet fuel, naphtha, fuel oil and everything in between, the Russian petrostate, as of the first week of July 2026, can no longer satisfy its own market.

Treat the above weekly numbers as a moving target.

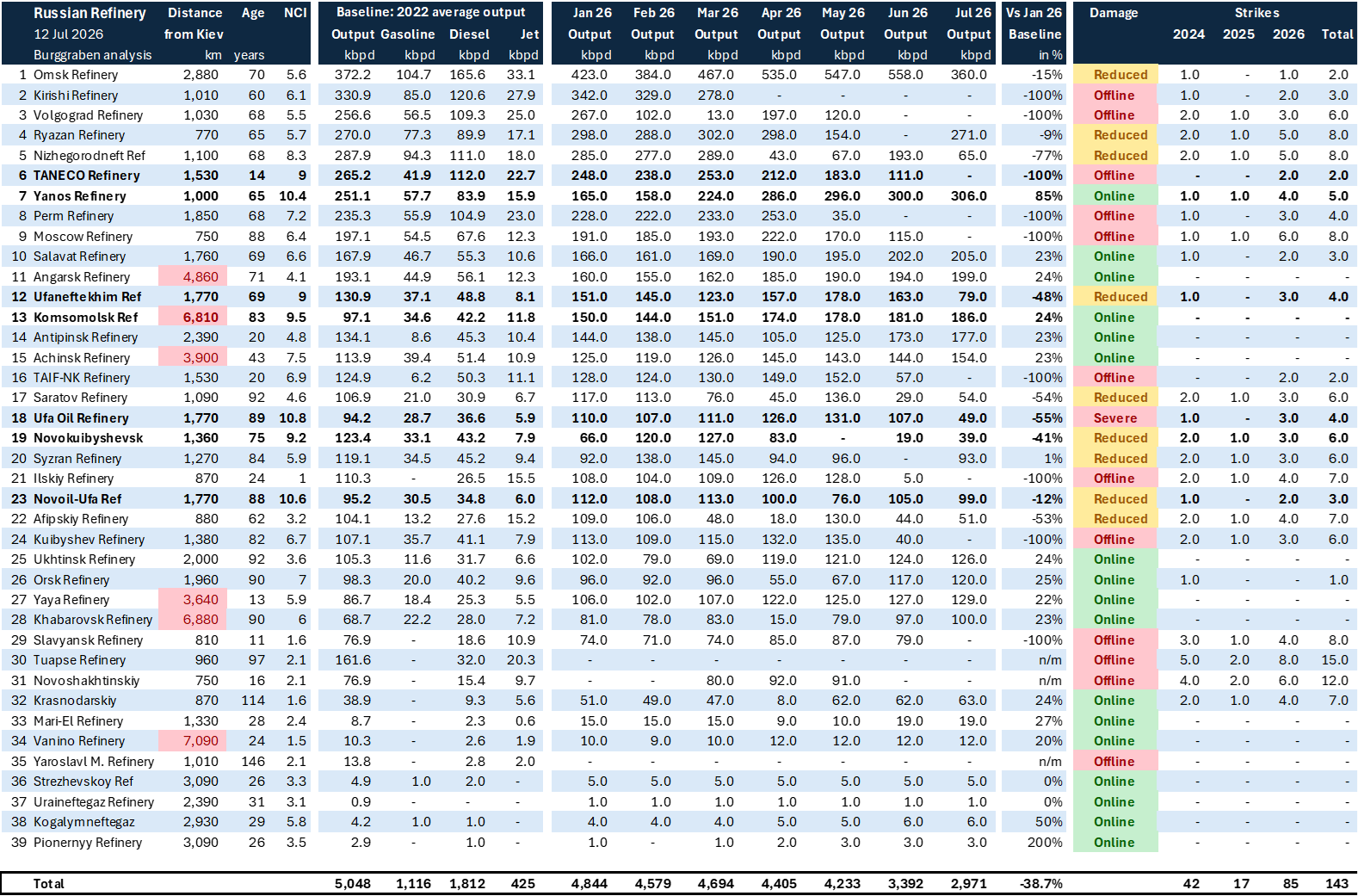

We do not, and cannot, know precisely how severe the damage is at every refinery. We simply do not possess the refinery-by-refinery high-resolution satellite imagery produced by firms such as Vantor. Even then, it would often remain impossible to determine whether a crude distillation unit was hit directly or merely caught fire as a consequence of damage elsewhere. Fortunately, we do not have to rely on satellite imagery alone.

Besides our refinery balances, we watch Russia’s exports closely. They provide an elegant back-test. If a drone destroys the CDU, the crude distillation unit, the large distillation tower that sits at the front of every refinery, the plant can no longer process crude oil. Refinery throughput falls and those barrels leave the country as crude instead. We observe exactly that.

Kpler data show seaborne crude exports exploding from 3.4mbpd in January 2026 to 4.6mbpd in June. At the same time, Russian crude discounts have widened sharply, with August-loading Urals into India trading at discounts exceeding US$10/bbl, among the widest since before the Iran conflict.

Taken together, the conclusion is straightforward. Our export back-test confirms that at least 1.2mbpd of Russian crude can no longer be processed domestically. Naturally, exports lag refinery outages by roughly two to three weeks, making the July and August export data particularly important following the latest wave of Ukrainian strikes.

The same logic applies to every major refining unit.

Hit the reformer and gasoline production falls while, assuming the CDU continues operating, naphtha exports rise. Hit the fluid catalytic cracker (FCC) and gasoline production falls further. Hit the hydrocracker and diesel output collapses. Many Russian refineries remain relatively simple facilities with low Nelson Complexity Index (NCI) ratings, making these relationships comparatively easy to identify through changing export patterns.

Two important conclusions follow. First, secondary processing units take far longer to repair than a CDU. Their components are substantially more complex and, under sanctions, far harder to replace. Second, restarting crude processing does not mean motorists receive more fuel. Crude throughput may recover while the gasoline and diesel units remain offline for months. Rising refinery runs therefore tell us surprisingly little about what ultimately reaches the filling station. That is precisely why we prefer measuring actual product balances rather than headline refinery throughput.

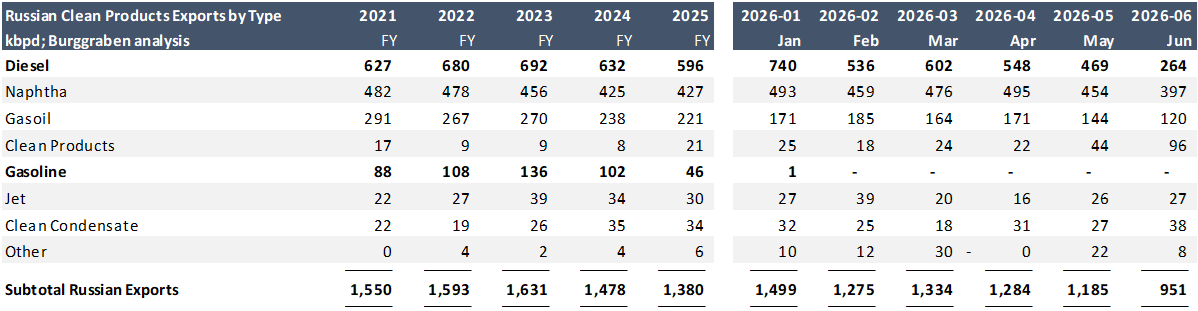

The verdict is clear. Gasoline is short. It was already heading in that direction before the latest drone campaign. Exports fell from 136kbpd in 2023 to 102kbpd in 2024, then to just 46kbpd in 2025, before collapsing to effectively zero under the 2026 export ban.

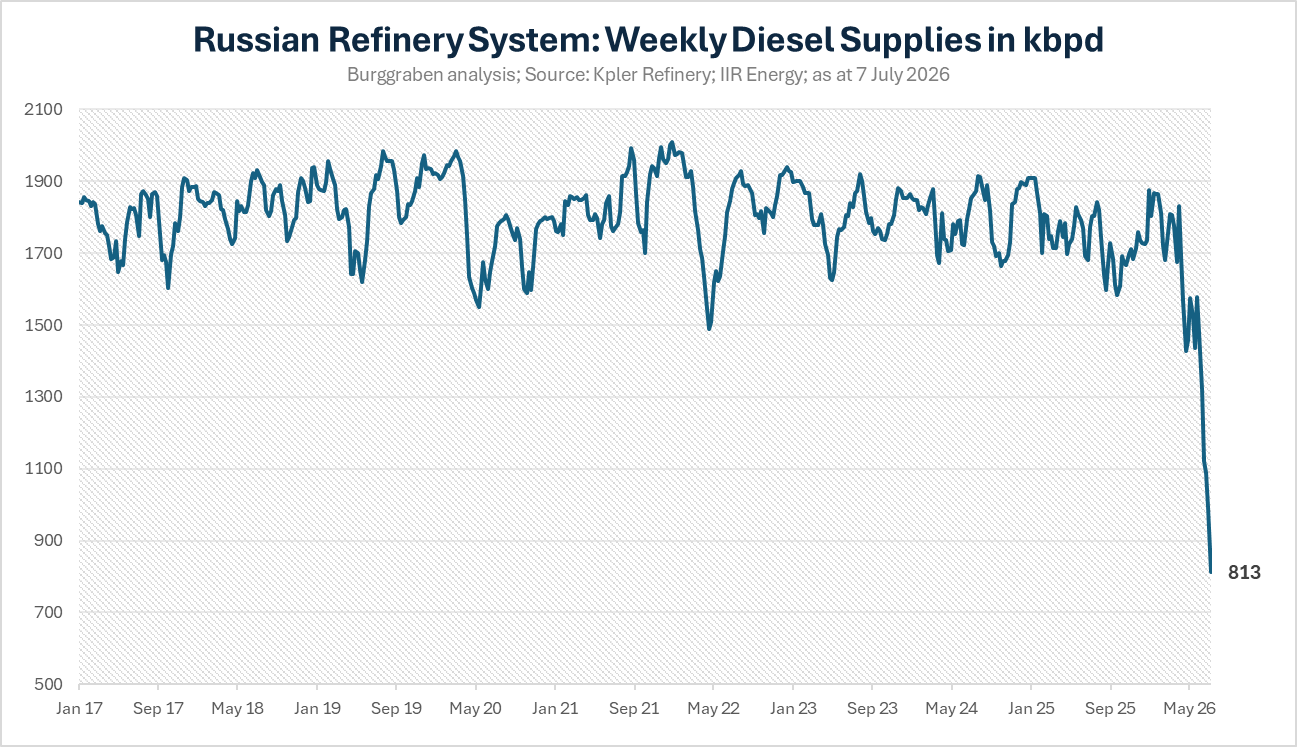

The more interesting story is diesel. Russian diesel exports have now collapsed as well. Combining diesel and gasoil, exports have fallen to roughly 400kbpd from around 910kbpd as recently as January. Those exports are now effectively banned too.

Naphtha has proved the most resilient product so far, declining only modestly from 427kbpd during 2025 to 397kbpd in June. Even there, however, exports continue to move lower. The damage is therefore no longer confined to one refinery or one product stream. It is broad-based across the entire clean-product barrel.

Ultimately, the tell is not any individual drone strike.

It is that the Kremlin is now looking at gasoline imports while simultaneously preparing to lower domestic fuel specifications. Governments do not import fuel or debase fuel quality unless their domestic fuel balance has fundamentally broken down.

Roughly 44% of Russian refining capacity was offline during the first week of July. That number will move. The conclusion will not.

Gasoline - A Volume & Behavioural Issue

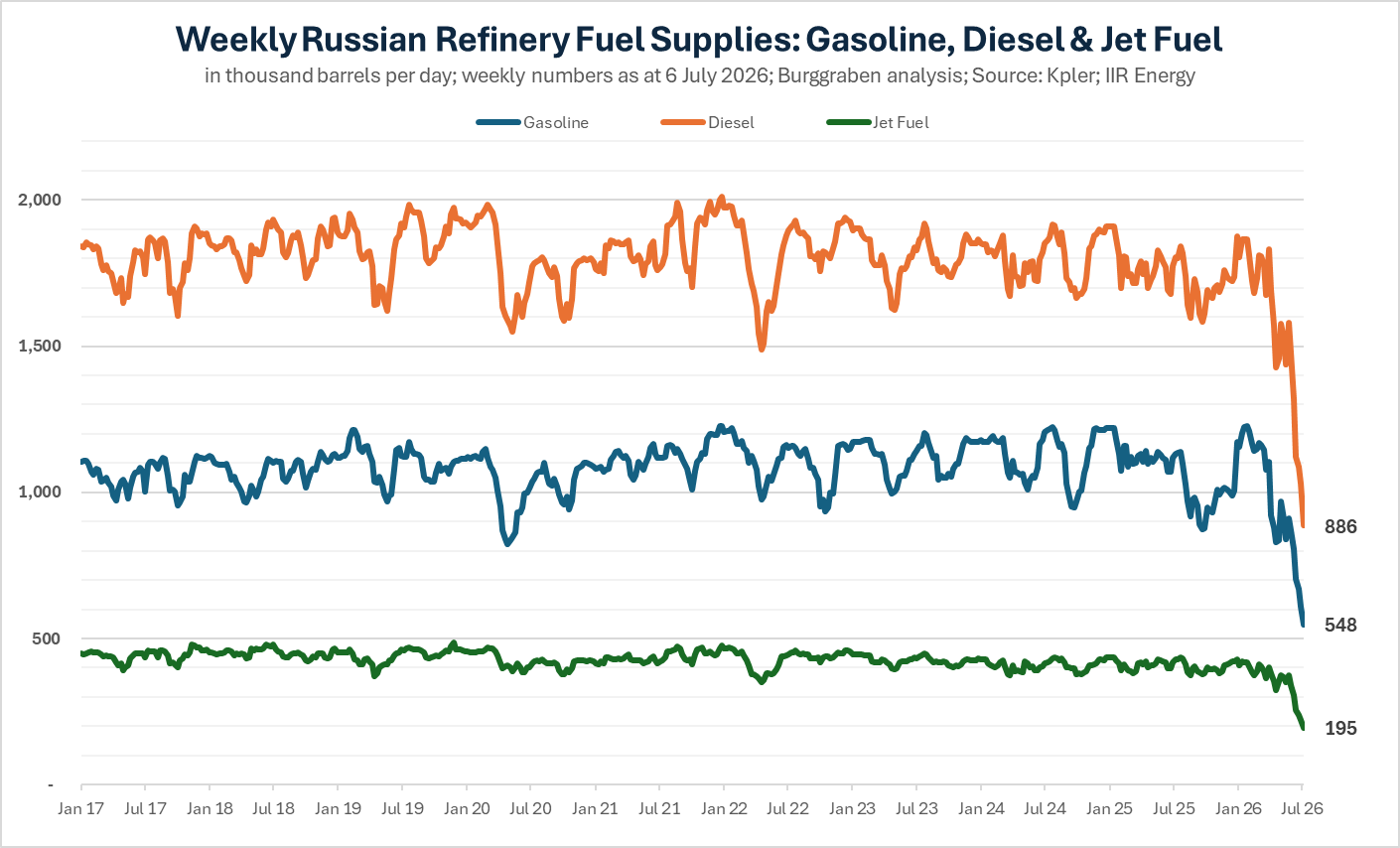

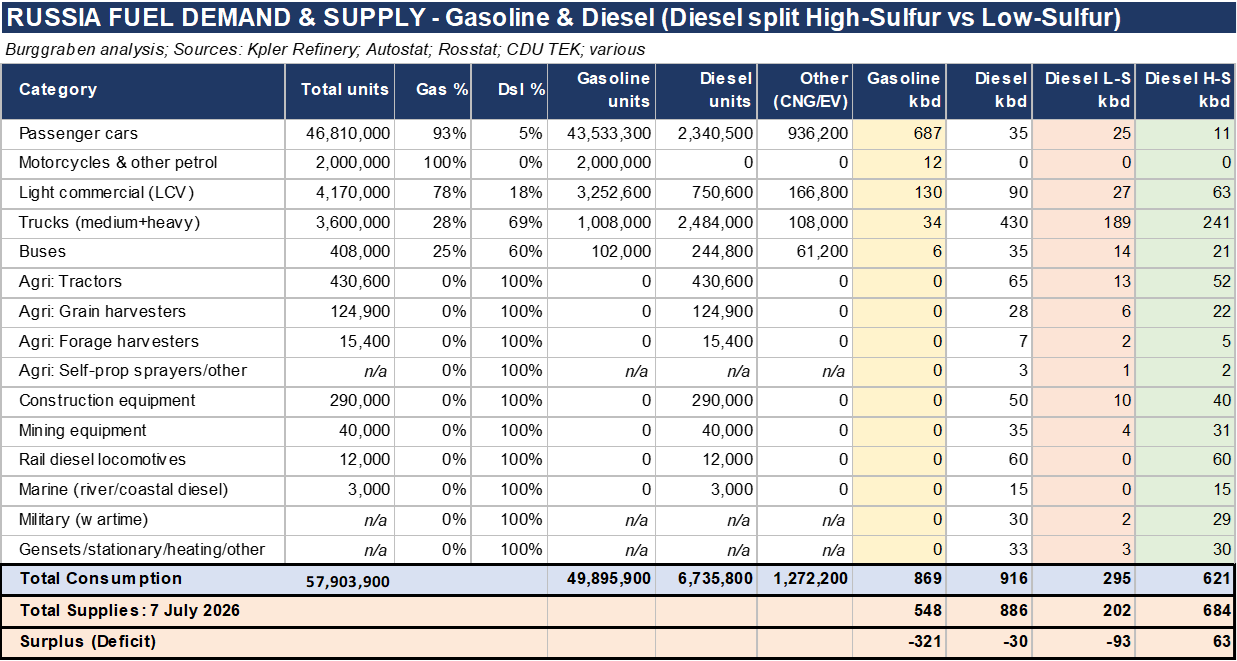

As at 7 July 2026, Russia’s refinery system was short roughly 320kbpd of gasoline against domestic demand of around 880kbpd.

The human consequences are already becoming visible, and here the outside record is worth quoting. On 6 July, the Institute for the Study of War (ISW) documented that intensifying gasoline shortages across Russia and occupied Ukraine are now materially affecting the daily lives of ordinary citizens.

The number of Russian federal subjects experiencing shortages and fuel rationing has climbed steadily since mid-June, with shortages in occupied Crimea beginning as early as May. As supply tightened, prices rose and queues lengthened. Regional governments and filling station operators responded by imposing gasoline and diesel purchasing limits in an attempt to contain the inevitable panic buying.

According to ISW, approximately 78 of Russia’s 83 federal subjects have now experienced fuel shortages, while authorities in 48 have imposed official gasoline or diesel purchasing limits.

Our own data suggest the situation is deteriorating further. Even before incorporating the latest strikes on Omsk and YANOS, weekly gasoline production has already broken below the critical 700kbpd threshold against a non-seasonally-adjusted consumption baseline of roughly 880kbpd. Summer demand, what Americans call the driving season, pushes actual consumption higher still.

There is no doubt panic buying is now amplifying the crisis. But that is not a bug of a supply crisis. It is a feature of every supply crisis. Once households lose confidence that fuel will be available tomorrow, they buy more today. No government has ever managed to legislate that psychology away.

Our real-time refinery balances, however, make one thing abundantly clear. The panic is a consequence, not the cause. Russia has a gasoline shortage because it lacks gasoline.

Back-test - GdeBENZ: Where Is The Benzin?

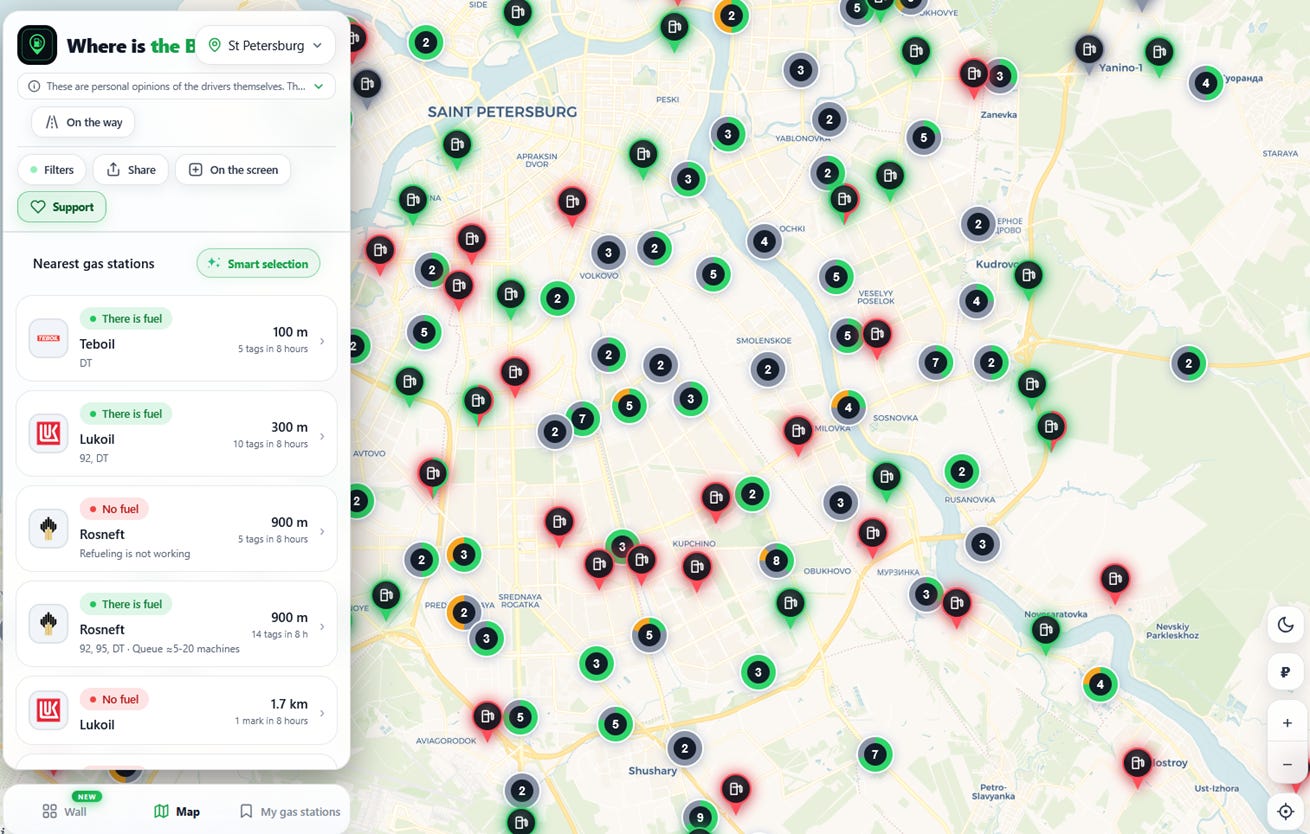

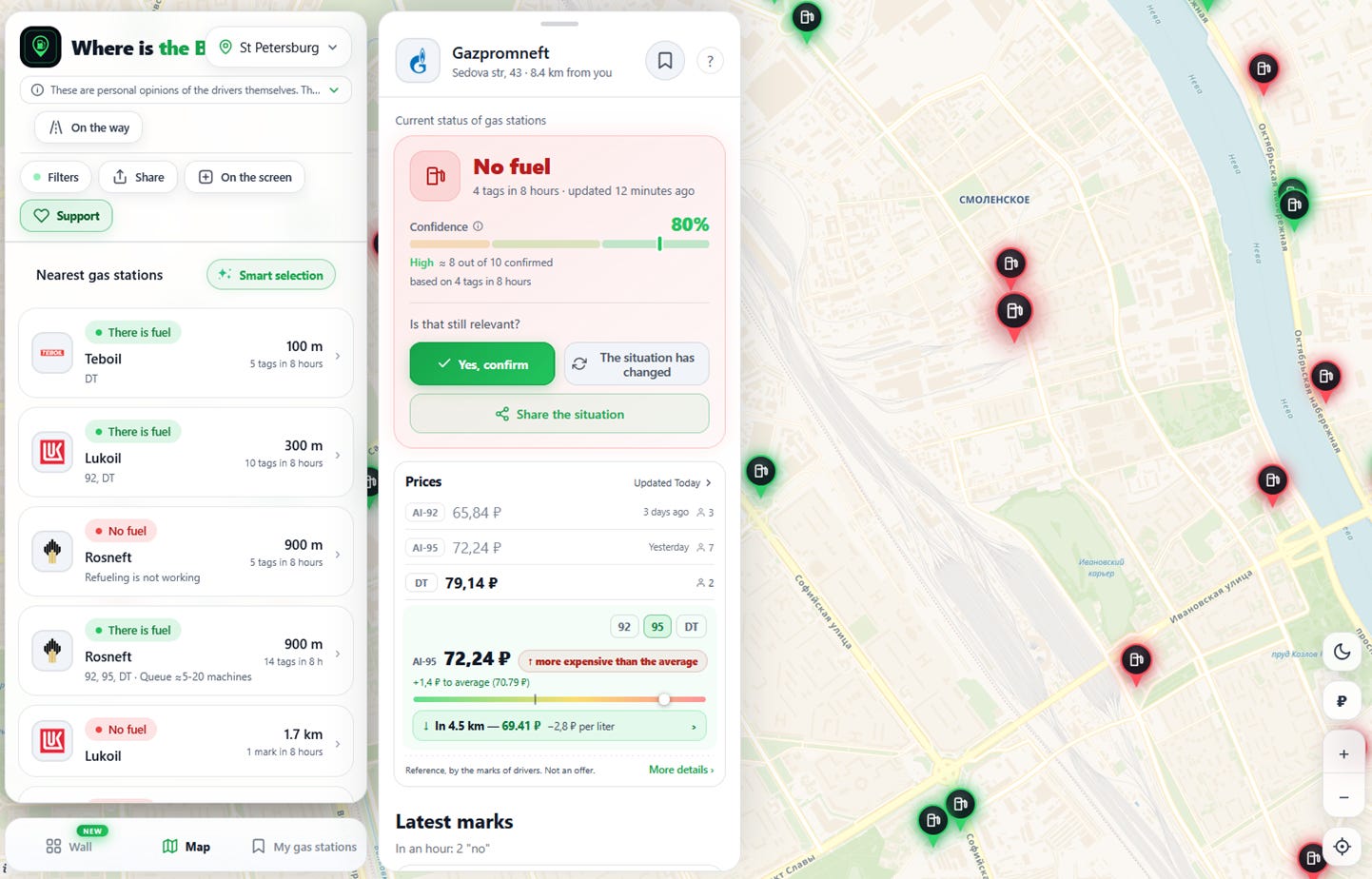

In June 2026, Russian programmer Evgeny Chudov launched GdeBENZ, a crowdsourced “people’s map” of Russian filling stations. Drivers report whether stations are open or empty and estimate queue lengths in five categories, ranging from fewer than five vehicles to more than one hundred.

The site exploded in popularity, reportedly attracting more than 812,000 unique visitors and generating around 100,000 station reports within forty-eight hours, according to Vedomosti Ural. Naturally, the data are imperfect. No registration is required and Ukrainian activists quickly began submitting false reports through VPN connections. This is, after all, an information war as much as a conventional one.

Individual station reports should therefore be treated with caution. The aggregated city-level picture, however, is surprisingly robust. Janis Kluge scraped the data, or at least published the aggregated results, and they tell exactly the same story as our refinery balances.

The problem is volume.

Other services are now emerging as well, including Yandex. They would not exist if, as the Kremlin continues to insist, everything were under control. Feel free to try them yourself.

Notice the 30-litre purchase limit shown in the screenshot above. Every station I checked displayed the same restriction. That independently confirms what local media have been reporting for weeks.

We have now launched our own automated data scraping across roughly 200 Russian cities and will report the results as they become available. Whether these services remain accessible from Western IP addresses is another question entirely.

For now, the picture is already remarkably clear. AI-98 is effectively unavailable across most major Russian cities. Diesel is becoming increasingly difficult to obtain as well, despite what various Russian commentators on X continue to claim.

The situation is not “manageable.” It is exceptionally bad.

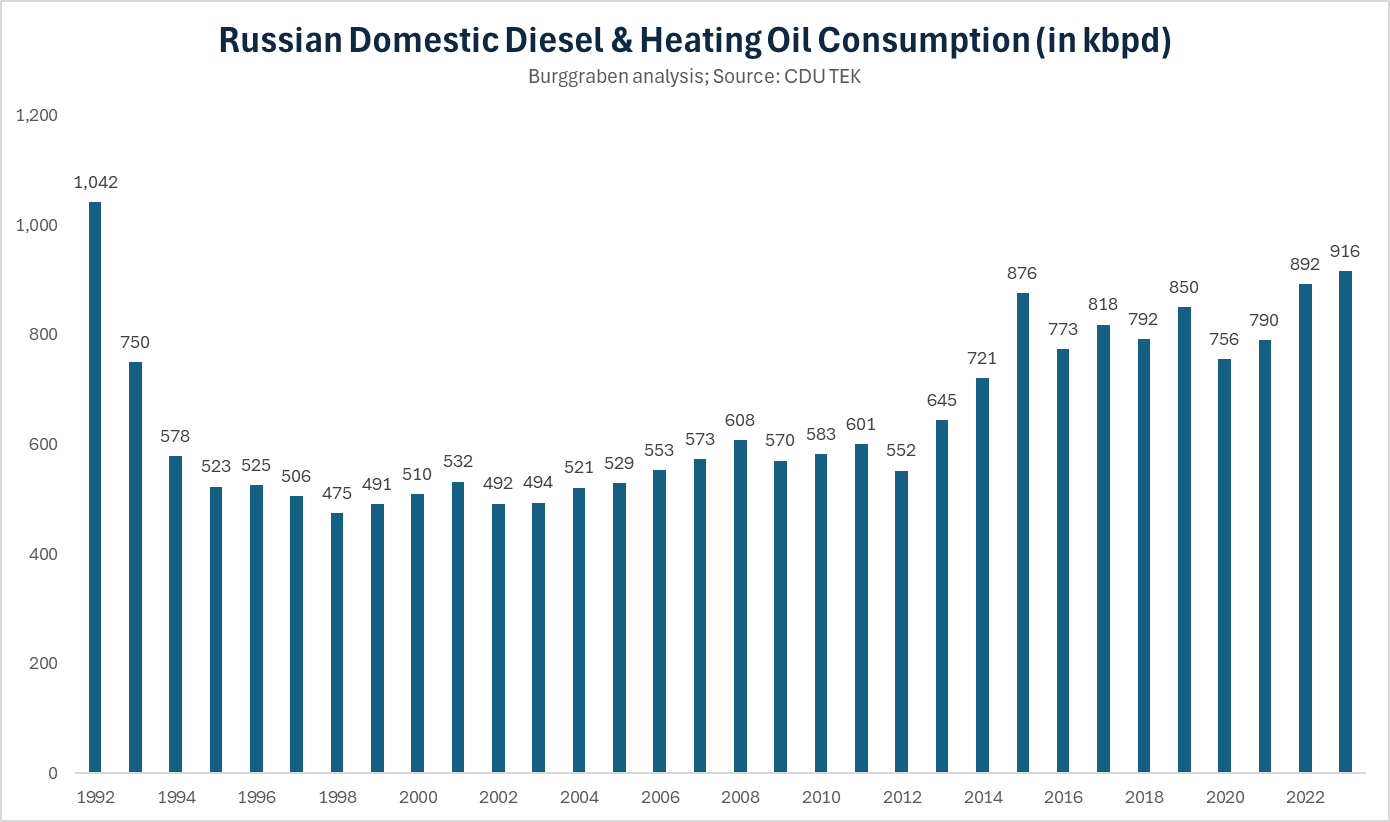

Diesel - A Volume & Behavioural Issue

Diesel has now become the more complicated story and, arguably, the more dangerous one.

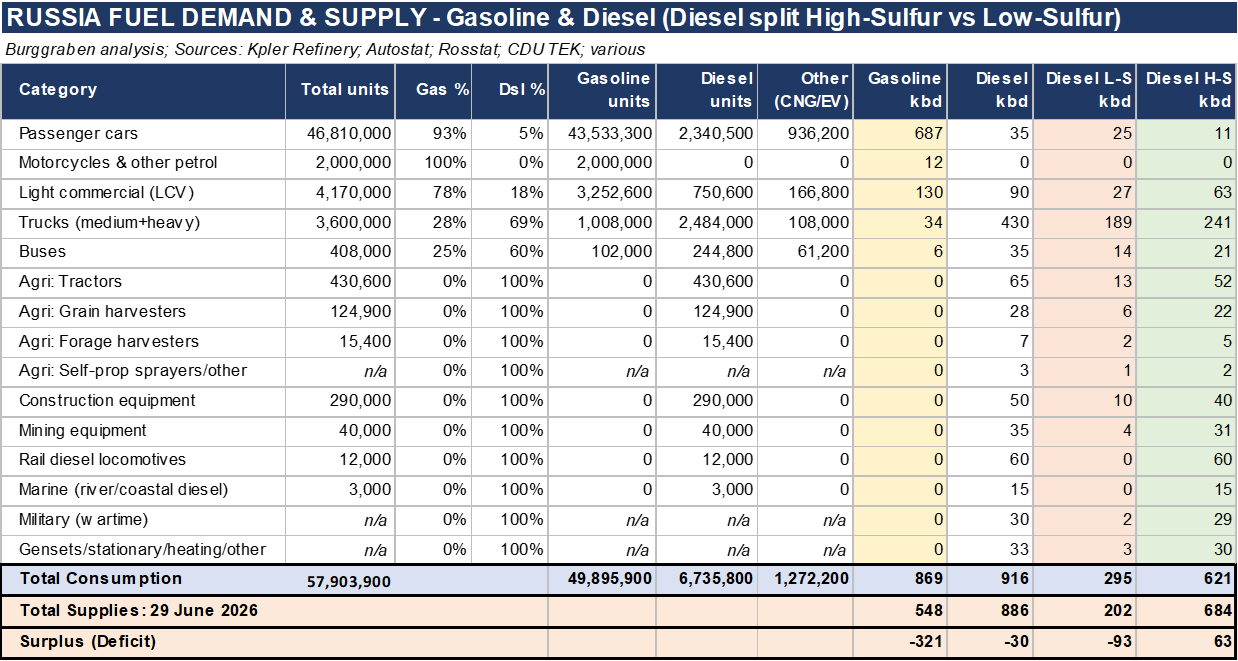

Unlike gasoline, diesel is not a single market. It splits into low- and high-sulfur grades serving very different parts of the economy. Low-sulfur diesel powers most modern trucks, agricultural machinery and heavy equipment. High-sulfur diesel still finds its way into older machinery, locomotives, power generation and marine applications. Understanding that distinction matters because Russia is now running short of both.

Our latest balances indicate domestic diesel supply has fallen below demand by roughly 30kbpd overall. Within that headline number the picture is considerably worse for low-sulfur diesel, where the deficit has widened to around 93kbpd, partly offset by a surplus of roughly 63kbpd of high-sulfur grades that cannot simply replace it. Diesel has therefore crossed the same line gasoline crossed weeks ago. The shortage is now real.

Russian diesel demand averages roughly 920kbpd, but unlike gasoline it is highly seasonal. Harvesting is now beginning across southern Russia, precisely when agricultural fuel demand accelerates. Since the Ministry of Energy stopped publishing monthly consumption figures years ago, nobody outside the government knows the exact seasonal profile. We will not pretend to a precision the data do not support. What we do know is that the market has become materially tighter than official statistics suggest.

That tightening creates something even more dangerous than a physical shortage. It creates incentives. And in Russia, incentives matter even more than in the West.

Once diesel becomes scarce, behaviour changes. Farmers stop trusting deliveries. Traders begin withholding supply. Middlemen start rationing access. Buyers pay whatever it takes because they have no alternative. Panic buying is not a bug of every supply crisis. It is a feature. In Russia, however, another force enters the equation: corruption.

Nowhere is that more visible than in the agricultural regions of southern Russia. According to the independent Russian outlet Pole Zreniya (”Field of View”; link), farmers increasingly report that diesel exists, but only for those willing to pay the panic price. One representative of a federal farming association summarised the situation succinctly:

“There is diesel. But they want to sell it dear. Purely on panic. A cartel agreement. They withhold volumes and release them through selected commercial intermediaries. Just like masks during COVID. Just like buckwheat. Just like sugar.”

That single quotation captures today’s diesel market remarkably well. Take Sergei Grechishchev, who farms in Kuban’s Yeysk district. As prices climbed through June, he finally accepted 104 roubles per litre and transferred roughly three million roubles to secure enough diesel for the harvest. Days later his supplier called.

“I’m going to disappoint you. Your allocation has been cancelled. The fuel simply isn’t there.”

His money remained with the supplier. The fuel, however, suddenly reappeared at 136,000 roubles per tonne. By the time he arrived home, the asking price had risen again to 142,000.

Most Russian farmers never buy directly from refineries. They buy through intermediaries who acquire refinery volumes on the SPIMEX commodity exchange before reselling them in smaller parcels at whatever panic pricing the market will bear. The script barely changes.

“You agree a price,” one farmer named Tatyana explained. “Two days later they call back. There is no fuel. Or we can still deliver... but at a higher price.”

Diesel in her district has reached around 148,000 roubles per tonne, equivalent to roughly 128 roubles per litre, more than double winter levels.

Going directly to refiners offers little protection. One 5,000-hectare farm in Rostov held a supply agreement with a Lukoil subsidiary covering sixty cubic metres. Deliveries stopped altogether at the end of May. Retail depots refuse to fill containers. Filling stations allow tractors to fill their tanks but prohibit filling portable drums.

Farmers therefore resort to absurdity. Some drive combines directly to filling stations. Others send employees at night carrying cash and empty barrels, hoping sympathetic attendants quietly dispense one hundred litres at a time while risking dismissal. Meanwhile a single combine may consume five hundred litres every day during harvest.

The market itself tells the story. Apply for diesel under the official “preferential” programme at around 70 roubles per litre and delivery may arrive “in August” or “whenever available” after full prepayment. Offer today’s market price instead and the fuel suddenly materialises almost immediately.

One farmer drew the obvious conclusion. “It feels like somebody has created an artificial shortage.” He is almost certainly right.

The state’s response has been largely theatrical. The Ministry of Energy insists supplies fully satisfy agricultural demand. The Federal Anti-Monopoly Service recommends “responsible pricing”. President Putin says he understands the difficulties and orders delivery schedules to be respected. None of those statements puts diesel into a tractor.

Meanwhile the economics deteriorate rapidly. Fuel costs that previously amounted to roughly 5,000 roubles per hectare have doubled towards 10,000, while grain prices have barely moved. As one farmer observed, production costs are rapidly converging with selling prices. Yet they continue buying. They have no choice. Harvest waits for nobody.

This is where today’s diesel market differs from the one we analysed only weeks ago. Back then behaviour mattered more than outright shortages. Today both matter.

Russia is simultaneously experiencing genuine physical deficits and the behavioural distortions that inevitably accompany them. The two reinforce one another. Every litre withheld by intermediaries deepens the shortage. Every rumour generates another wave of panic buying. Every queue convinces somebody else to fill every available tank.

Rick Stainton, a friend on X who spent a decade farming and operating businesses through Zimbabwe’s fuel crises, summed it up better than most economists ever could.

“It stops being a fuel shortage and becomes a thriving black market full of middlemen.”

Exactly. The tragedy is not merely that farmers pay more for diesel. It is that they gradually stop being farmers. They become fuel traders.

That is how fuel shortages corrode an economy. They do not simply reduce output. They redirect entrepreneurial effort away from producing wealth and towards securing access to scarce resources. Russia has now entered that phase.

When Size Becomes the Problem, Not the Advantage

Russia’s vastness is usually portrayed as one of its greatest strategic advantages: eleven time zones, almost limitless natural resources and enormous strategic depth. In a fuel crisis, however, those advantages work in reverse. Nearly everything in Russia moves by road across enormous distances, and roads run on diesel. A fuel shortage in a country this large is not merely a queue at the local filling station. It becomes a tax on every kilometre of the economy.

The trucking market is where the damage appears first. According to Kommersant [link], spot freight requests quadrupled within a single week as shippers scrambled for available capacity, while the supply of trucks contracted because drivers increasingly refused routes they could no longer guarantee to complete. Freight tariffs jumped roughly 10% in a week alone, and market participants expect further increases. The binding constraint is no longer price but availability. Carriers are reaching regional fuel purchasing limits, forcing them to reroute, postpone or cancel deliveries altogether.

The structure of the market is beginning to buckle as well. Roughly 70% of Russian road freight normally operates under long-term contracts. Those agreements are now being reopened despite cargo volumes remaining broadly unchanged. Shippers increasingly consolidate multiple customers’ goods into a single truck, while contracts that once ran for a year are renegotiated monthly simply to lock in prices for a few weeks. That is what a market looks like when it loses the ability to plan.

The disruption is spreading rapidly through the wider economy. Public transport, taxis and aviation are all feeling the strain. In some regions taxi drivers are simply leaving the road because they either cannot obtain fuel or would operate at a loss. Freight rates into occupied Crimea have reportedly increased by three to six times, reaching as much as RUB1.2 million per truck. Since transport costs are embedded in virtually every product sold, economists interviewed by The Insider [link] warn that the fuel crisis will feed directly into inflation across almost the entire economy.

Will This Normalise Quickly?

I doubt it.

What strikes me most about modern drone warfare is not the drones themselves but the economics they create. Ukraine no longer needs to destroy Russia’s refining system. It merely has to damage it faster than Russia can repair it. That is a profoundly different type of war.

A chemical engineer recently made an observation on X that caught my attention [link]. Watching footage from Omsk and several other refineries, he pointed out that the facilities were clearly operating normally when the drones arrived. Columns and pipelines were still full of hydrocarbons and the entire system remained under pressure. Under those conditions, even a relatively small drone can trigger secondary explosions and fires that destroy equipment worth hundreds of millions of dollars and take months, sometimes years, to replace under sanctions.

That should not have happened. Every refinery has emergency shutdown procedures. In the event of an imminent attack, operators can isolate processing units, stop hydrocarbon flows and depressurise the system by routing hydrocarbons to the flare. An emergency shutdown is disruptive and costly, but it dramatically limits the damage if a strike follows.

Omsk raises an obvious question. Ukrainian Fire Point FP-1 drones cruise at roughly 200km/h. A flight from the Ukrainian border to Omsk, around 2,500 kilometres, therefore takes well over twelve hours. Russia’s air-defence network does not need to shoot every drone down. It merely has to detect them early enough to warn the target refinery that an attack is coming. Yet the repeated footage suggests exactly the opposite. Refineries continue operating until impact.

Whether that reflects failures in radar coverage, command and control, communication or simple complacency hardly matters. The result is the same. Russia is allowing billion-dollar industrial assets to absorb maximum damage from drones carrying warheads that cost a tiny fraction of that amount. That is why I do not expect this crisis to disappear quickly. Remember the “brains” comment by Khodorkovsky (link)?

Ukraine has discovered a remarkably favourable exchange ratio. It does not have to destroy Russia’s refining system. It merely has to keep it permanently off balance. In a country spanning eleven time zones, defending every refinery, every fuel depot and every piece of critical energy infrastructure against cheap, long-range drones is an almost impossible task. Repair crews will spend years chasing damage that Ukraine can recreate overnight. That is a war of economics as much as one of technology, and, so right now, Ukraine is winning it.

Imports to the Rescue?

Khodorkovsky (link) is right that imports can cushion Russia’s gasoline deficit. But I argue they cannot solve it.

To close the gap, Russia needs gasoline that clears four hurdles simultaneously. It must be unsanctioned, surplus to the exporter’s own domestic market, available in meaningful volumes and cheap enough to make the trade commercially viable. Clear all four at once and the list of candidates becomes remarkably short, both on land and at sea.

Let’s start at the top of the market and watch the options disappear.

The world’s two largest gasoline exporters, the EU-28 and the United States, are immediately ruled out. Europe remains by far the largest net gasoline exporter globally, while the United States supplies not only Mexico but much of Latin America. Both have imposed comprehensive petroleum-product sanctions on Russia (here & here). That removes the largest part of the global export market at a stroke.

Even if one entertains the fantasy that Brussels lifted sanctions as part of a future peace agreement, the trade still would not work. Russian domestic gasoline prices are simply too low.

That brings us to the second filter, and arguably the more important one. Russia’s domestic gasoline is cheaper than almost anywhere else. Cheaper than China, the only country with genuine spare refining capacity. Cheaper than India, the world’s third-largest gasoline exporter. Cheaper than Turkey, Pakistan, Malaysia and Mexico. Only a handful of Middle Eastern and African petrostates sell gasoline below Russian domestic prices.

No rational exporter voluntarily ships gasoline into a market priced below its own domestic parity.

The Middle East is often presented as the obvious solution. It is not.

Iran, despite being one of Moscow’s closest allies, exports virtually no gasoline. Decades of sanctions and chronic underinvestment have left its refining system unable to produce a meaningful export surplus. Iraq, Kuwait, Qatar and even the UAE are not major gasoline exporters either. Producing export-grade gasoline is considerably more difficult than exporting crude oil, requiring sophisticated secondary refining units that many hydrocarbon-rich countries still lack, even decades after nationalising the assets of the Seven Sisters.

That leaves Saudi Arabia and Oman. From Moscow’s perspective, those are the best-case scenario. Saudi Arabia exports gasoline from the Red Sea, safely outside the Strait of Hormuz, while Oman sits outside the Strait altogether. Their export infrastructure is among the most secure in the world.

Unfortunately for the Kremlin, that is where the good news ends.

Combined, Saudi Arabia and Oman exported roughly 180kbpd of gasoline during June 2026. That volume would certainly help Russia. It simply is not available.

Both countries already supply higher-paying, lower-risk customers across Singapore, the UAE, Egypt, Jordan, South Africa, Pakistan and elsewhere. Every cargo already has a home. Every buyer pays more than Russia can. With domestic gasoline prices among the lowest anywhere in the world, Russia has effectively priced itself out of the Middle Eastern gasoline market. It cannot outbid Karachi, let alone Singapore.

Even if the Kremlin chose to subsidise those imports, logistics would remain another formidable obstacle. Building a continuous gasoline bridge from the Gulf to sanctioned Russian ports such as Ust-Luga requires a clean-product tanker fleet Russia simply does not possess. That is a very different business from short-haul regional deliveries around the Gulf that take hours rather than weeks.

At best, Russia may attract the occasional opportunistic cargo. The Asian OECD export complex looks even less promising.

South Korea, Singapore and Taiwan already supply premium markets such as Australia, New Zealand, Indonesia, the Philippines, Malaysia and even California on the US West Coast. Those are mature, low-risk, dollar-denominated trades supported by decades of investment, efficient logistics and reliable counterparties.

Russia cannot compete. Not on price. Not on payment risk. Not on sanctions. Not on logistics. And certainly not with a clean-product tanker fleet it barely possesses.

None of this means Russia will import no gasoline. It almost certainly will. Belarus, Kazakhstan, opportunistic cargoes from India or the Gulf and the occasional politically motivated shipment will all help around the edges.

But they do not solve the problem. They merely buy time. The underlying deficit remains exactly where it started: inside Russia’s own refining system.

India - A Painkiller, Not a Cure

Now let us turn to India — the most-cited candidate, for good reasons.

India has a vast refining industry, capable of processing around 6mbpd of crude each day (excluding maintenance), with plenty of export capacity. That is what Russia requires. What is not ideal is that India carries a domestic gasoline price around 20% above Russia’s. So prima vista, the arb is closed.

However, India became the largest single buyer of Russian crude starting in 2022 — mostly Urals — besides China with imports well above 2mbpd and closer to 2.7mbpd in June 2026 alone, according to our real time data.

Therefore, the above set-up almost writes itself: a swap — Russian crude for Indian gasoline. It could let one or several Indian refiners buy at a discount to the already-discounted Urals-to-Brent, more than cover the cost of refining and freight, and hand Russia the finished product it can no longer make at home. Prima facie, an elegant fit.

And the trade is apparently already under way, according to this source which cites that Russia seek to import 400,000 metric tonnes of gasoline per month (111,000kbpd) from India - I assume for the time being, not as a one off. That would fit our June data.

That is roughly a third of India's gasoline exports to divert away from existing clients. A stretch — but perhaps a workable compromise. India's refinery complex runs at around 85% utilisation and may be able to push 5% harder to squeeze out an extra 50kbpd for the export trade, while Russia may be able to outbid some barrels from India's existing customers. After all, it too has a bit of leverage.

And let us not underestimate the pull of it: Indians like a good deal, and a subsidised, captive buyer at the other end of a short-ish sea lane is exactly the sort of trade Indian refiners are built to exploit.

However, let us now count the frictions — because this is not a story of one wall, but of many small ones stacked on top of each other. Death by a thousand cuts kind of thing. Who knows, but here are the issues I see coming:

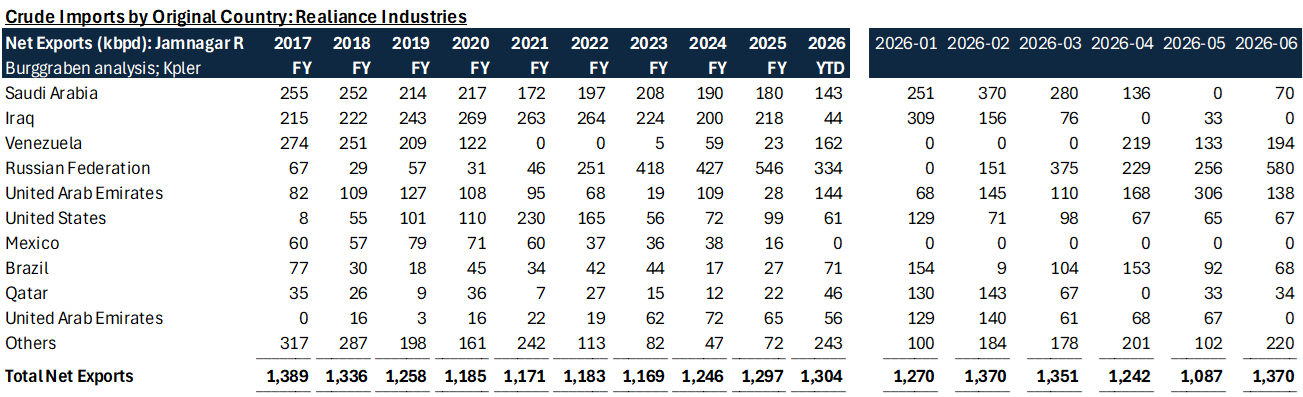

The first cut is the crude leg itself. To force Russia toward the negotiating table, the US tightened sanctions on any trade in Russian crude, and Urals purchases at Indian refiners duly fell. The local champion, Reliance Industries — India’s largest refiner by a distance — stopped buying from Russia altogether in January 2026 (table below), before resuming it through June; most others kept lifting, but at reduced volumes for a brief period of time.

Then, Trump alongside Israel, struck Iran in the spring of 2026 — functionally closing the Strait of Hormuz, sending crude spiking, and giving us a saga I have documented on this platform. The spike changed Washington’s calculus: to keep barrels moving and prices in check, the administration let more Russian oil flow, and handed Indian refiners — expressis verbis — a sanctions waiver to buy the Russian crude that had piled up in floating storage over the preceding months.

Which sets up the live question: does the Trump administration keep waiving? We do not know, and the topic will stay dynamic. The recent signals point to expiry rather than extension — officials, Secretary of State Marco Rubio among them, have stressed that the exemptions were strictly time-limited instruments, meant only to steady global energy markets through the initial Hormuz shock. But Rubio does not call the shots; Trump does, and he is fickle. So I keep an open mind. But crude sanction waivers is the first “cut” meaningful volumes must survive for Russia to fix its gasoline problem.

Now to the cut I think matters most — and it is really two cuts working together: the law and the ton-miles. Take the law first, because it is the one people miss. There is a world of difference between shipping Russian oil and petroleum products out and shipping gasoline in, and it is the whole ballgame.

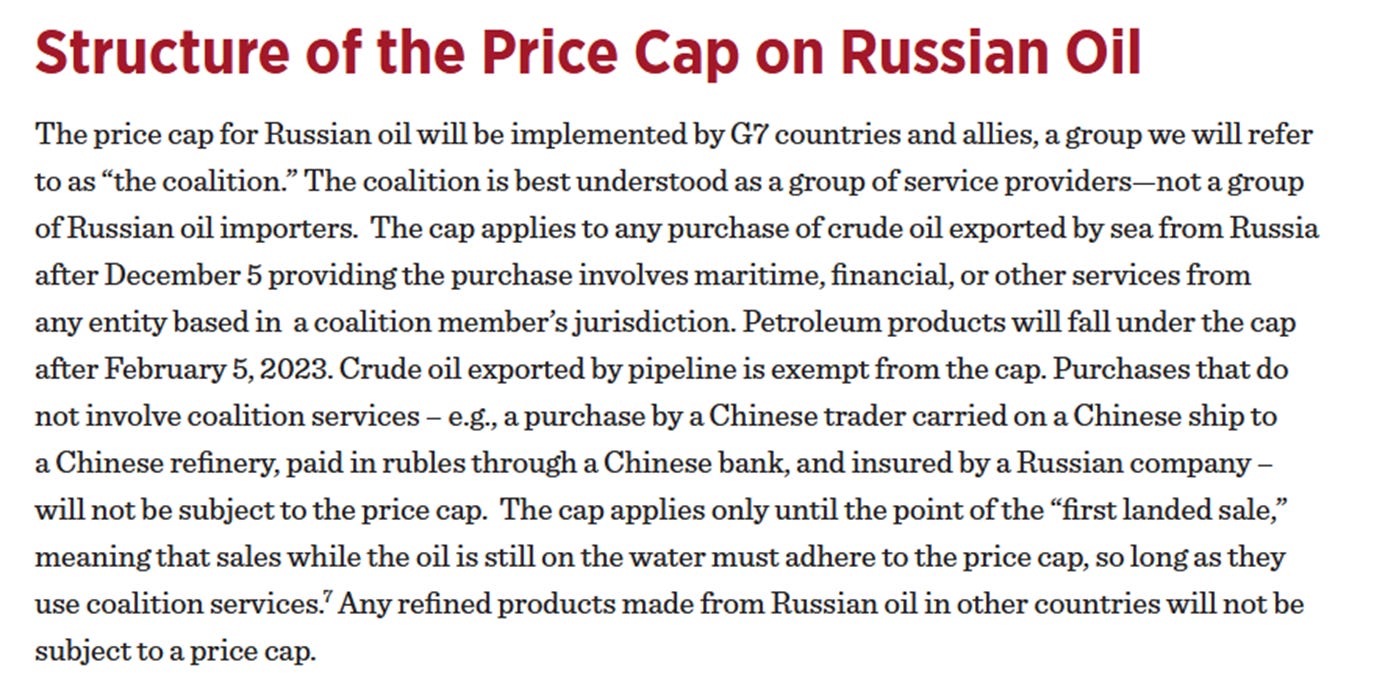

Sanctioned exports of Russian oil have a legal safe harbour — the G7 price cap. Carry Russian crude or product out below the capped price ($100/bbl for gasoline, diesel and kerosene; moving policy target) and a Greek vessel owner is doing permitted business.

That is how Dynacom, the Onassis group and their peers legally banked close to $4bn over three years hauling Russian oil, as the FT laid out this week. Legal, if not moral — and arguably moral too, in a roundabout way, since the cap was designed to keep Russian barrels flowing so world prices would not spike; the West wanting the oil moved, just not the Kremlin enriched. An uncomfortable trade-off, because nobody should be feeding a war machine. But it is legal, and it is a machine that exists.

Gasoline flowing into Russia has no such machine or, rather, price-cap channel that blesses it — only exposure: Russian ports, Russian counterparties, the EU’s tightening maritime-services net, and the reputational radioactivity that already saw Ukraine brand those same Greek owners “sponsors of war” for the export trade.

So the mainstream, insured, Western-serviced professional fleet — the fleet that does clean-product business every day — has every reason to look at this carefully and make a long-term risk, not a short-term profit judgement.

The tell is in how the cargoes actually move: Russia’s first jet-fuel imports are being laundered from Japan through South Korea “via a chain of intermediary companies,” and the Indian gasoline moves quietly, according to this article. You do not route a legal trade through cut-outs. So that is a first indication of where this is going.

But does that work at scale? Can Russia load enough gasoline it can buy in India each week to bring it back home? I don’t know. What I do know is that there is no established India-Russia gasoline import trade. Creating one means asking tanker owners to dedicate clean-product tonnage to a corridor with limited backhaul optionality.

That raises the freight required to make the trade economically attractive, and I mean substantially. It currently costs $5.34/bbl (about $3.4cent per liter or about 3-4% on current domestic quoted prices) to ship gasoline from Sikka in India to Chiba in Japan. Affordable. But what if that number goes up 10x because of dark-fleet economics and longer routes?

Back to the volume issue. One line of argument says Russia’s own gasoline and diesel export trade is now drying up fast, freeing tonnage for the import run. But that assumes the two are the same trade, legally. I do not think they are — and that difference is the whole point.

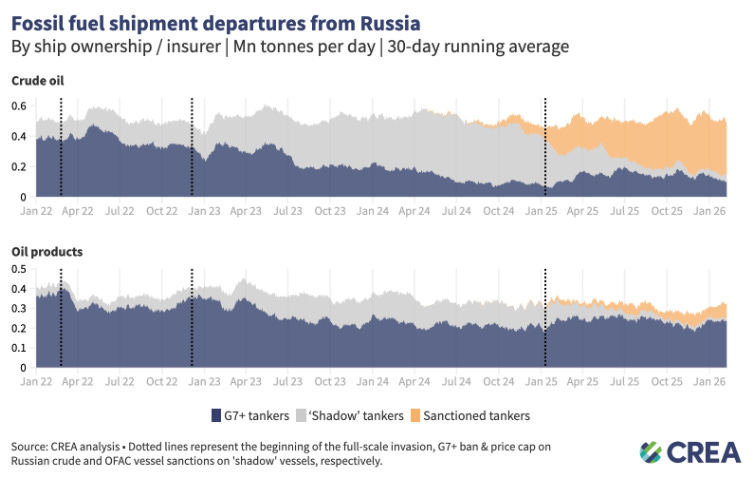

People will quickly point out that there is the dark fleet. True that but let’s look at the details more carefully: In February 2026, some 80% of the total value of Russian seaborne CRUDE oil was transported by ‘shadow’ tankers, while tankers owned or insured in countries implementing the price cap accounted for 19%. However, ‘Shadow’ tankers transporting PETROLEUM products such as gasoline handled only some 37% of Russia’s total volume of products. The remaining volume was shipped by tankers subject to the price cap policy.

Russia has now introduced an export ban for diesel too, not just gasoline, which may free up part of its dark fleet capacity used in the product trade. But Russia also continues to export other products such as dirty products. I guess my answer is, we will have to see how this will play out.

The most obvious line of argument is probably truer: among thousands of middlemen in the shipping industry there will always be an idiot keen to make a few dollars, and if that means scrubbing out a dirty dark tanker to load fuel into it, so be it.

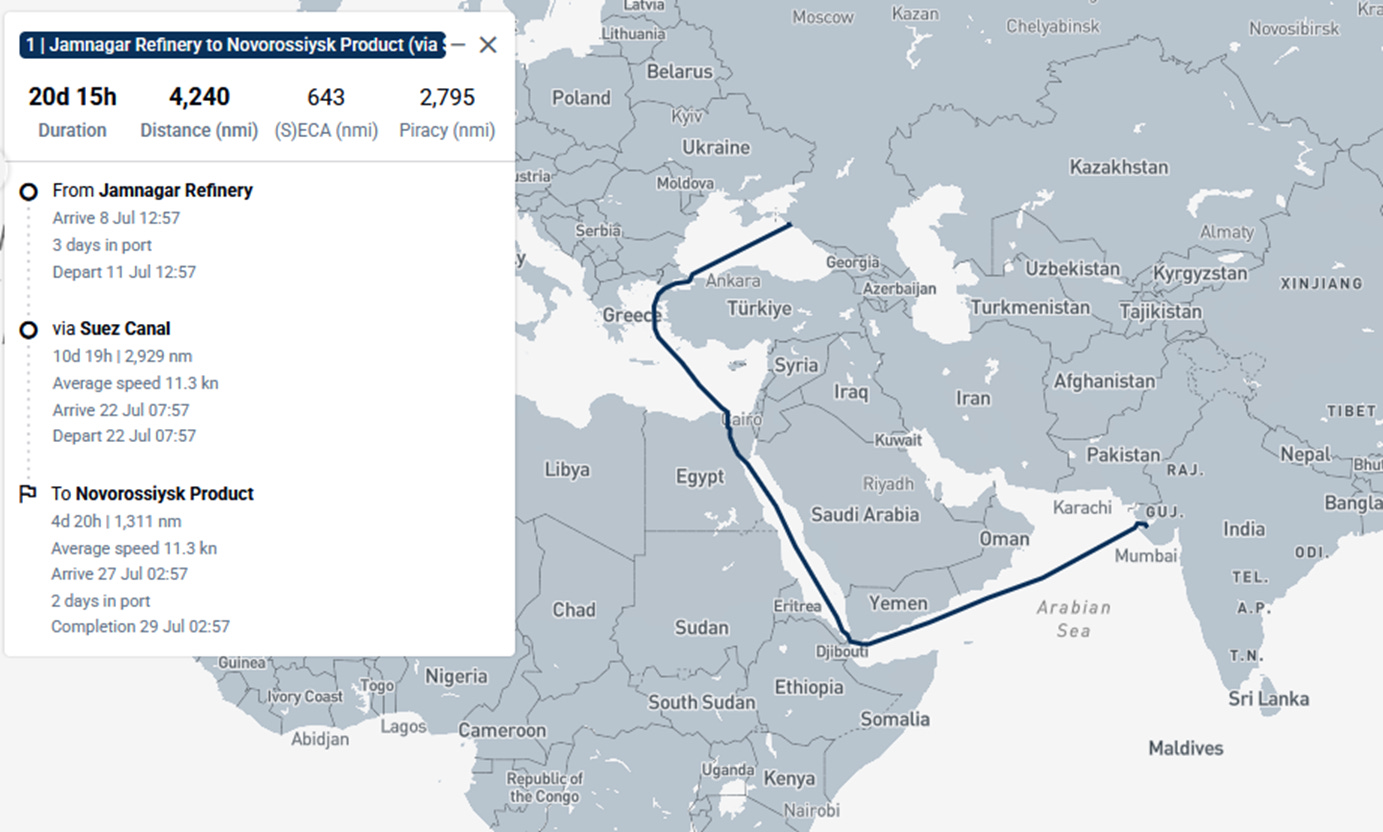

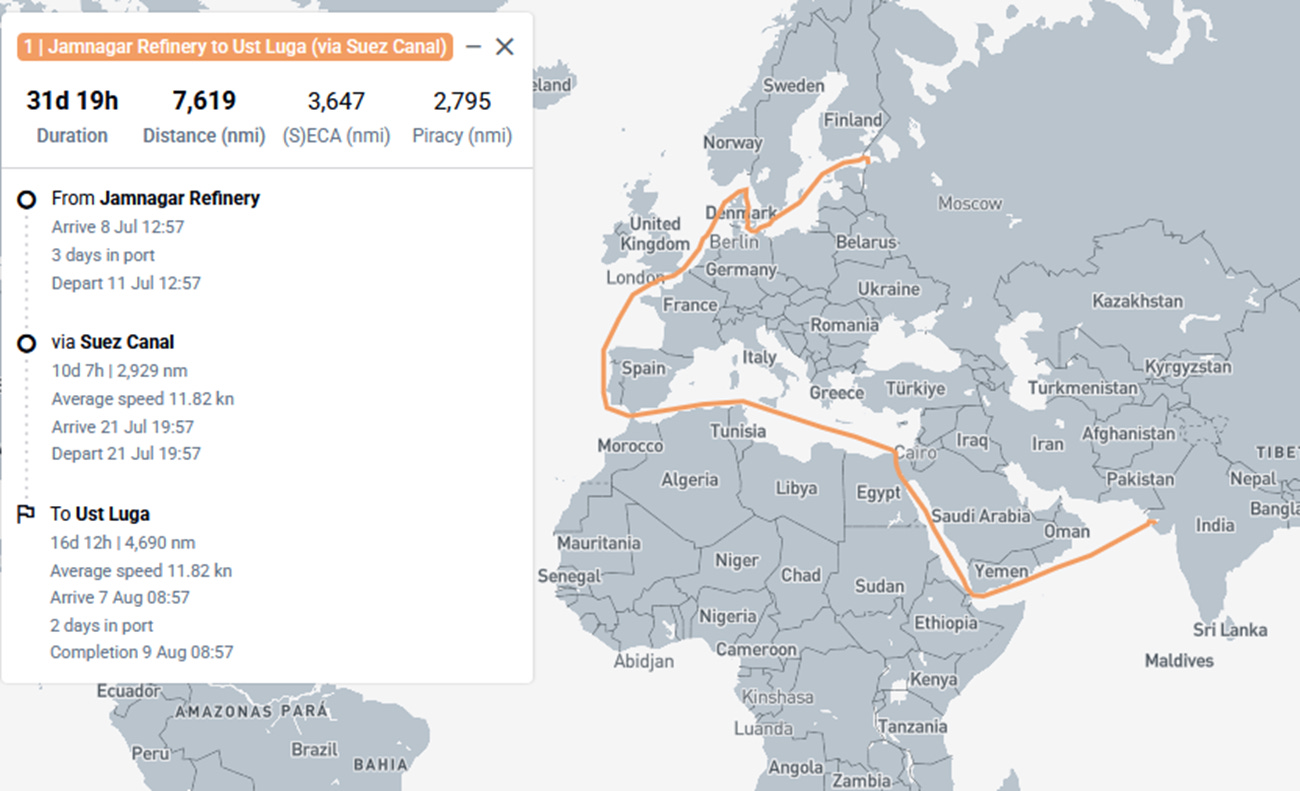

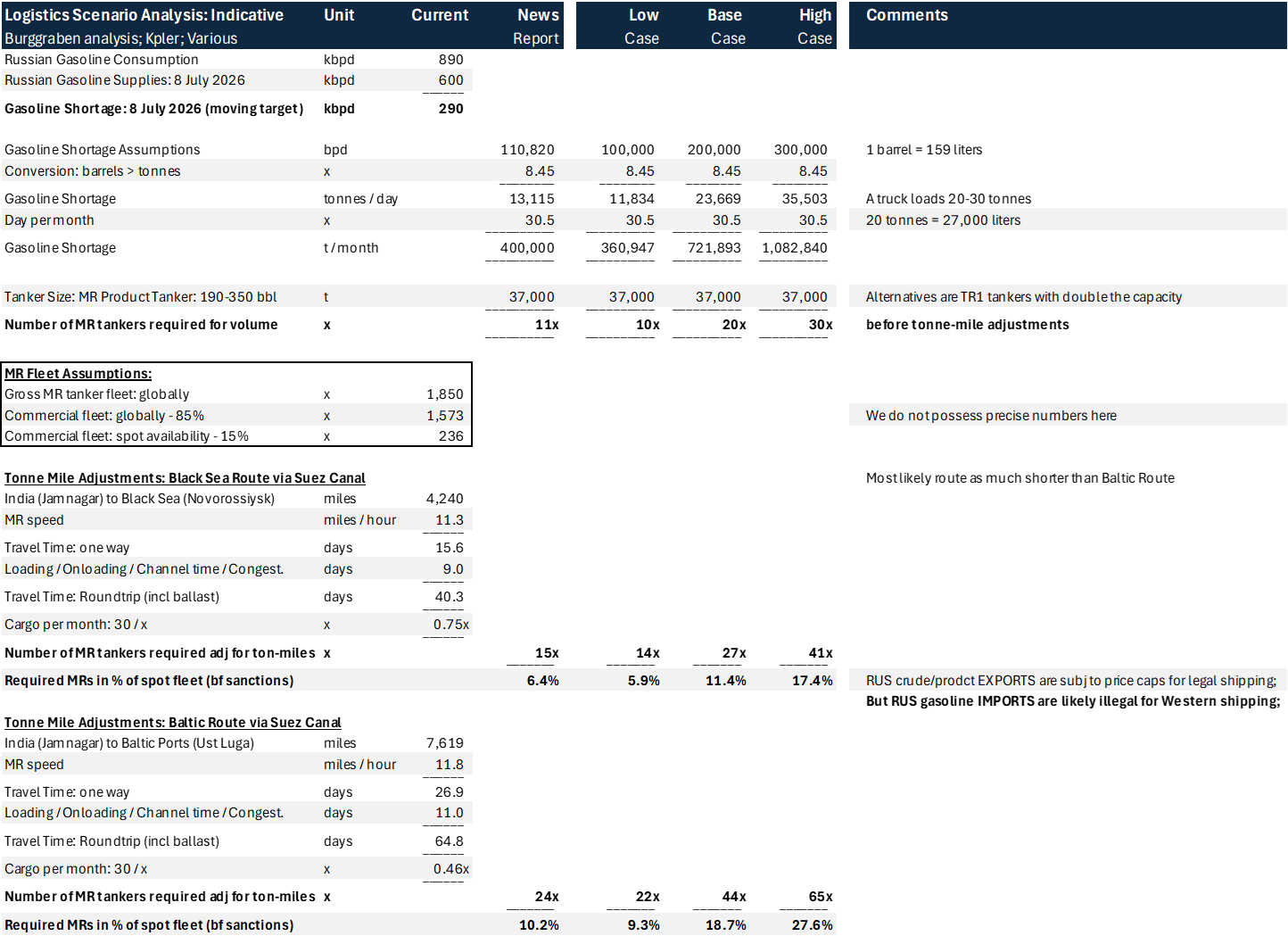

Personally, I think size matters most here. 100kbpd — roughly 11,900 tonnes a day, about 360,000 tonnes a month — is about ten MR cargoes a month in pure volume terms. Onto that goes the ton-mile multiplier. Indian gasoline must sail from Gujarat to Novorossiysk on the Black Sea (about 4,200 nautical miles via Suez), or at times to Ust-Luga on the Baltic (some 7,600) — a round-trip cycle of roughly 40 and 65 days respectively, once loading, canal and discharge are counted.

Stretch each cargo over that long a voyage and you no longer need ten ships; you need on the order of 15 held permanently on the Black Sea run, or north of 20 to Ust-Luga — call it something like 6% of the world’s spot-available MR tonnage, just for 100kbpd (see table below). That number is soft, but the direction is not: the distances are punishing, and they multiply every other constraint.

Because now combine the two. The ton-miles say you need a standing fleet; the law says the obvious fleet — the legal, London-insured, Western spot market — will not take the cargo. So you fall back on dark-fleet tonnage and the middlemen, as explained above. A few illegal loadings here and there. No problem.

But 20 MRs day in, day out, for months? I am less sure. Go to my high case in the table below and the requirement climbs to 40-65 tankers — perhaps as much as 38% of the MR spot fleet. That is a stretch. Move it to bigger vessels? Of course — but the same dynamics apply there too, in terms of availability.

Roughly half of Russia’s seaborne oil already moves on the shadow fleet, the G7-serviced fleet carrying most of the rest. Every shadow tanker pressed into carrying gasoline in is a tanker not lifting Russia’s crude out, at least in theory. The two fleets aren’t all interchangeable but you see my point.

Look, it took Russia 18 months to re-shuffle the crude and product trade back in 2022 when the tanker market was loose. Now it isn’t so much. Back then, the interests of the West and Russia were to give it time to adjust were aligned. Now? Not at all.

I do not believe anybody possesses enough knowledge of the dark fleet to answer that question with confidence but let me put it carefully: I’d be surprised if the global (dark) fleet can easily accomodate a 200,000 barrel per day petroleum product trade for months, let alone 300,000 - which is the direction of travel right now. Time will tell.

And another cut: the economics only work because the Russian oil companes pay for it (let’s call it the siloviki crooks). Imported gasoline lands above Russia’s capped domestic pump price, so Moscow is drafting Tax Code amendments to subsidise the importers — the Kremlin paying its own oil companies to bring in fuel it cannot sell at a profit.

Savour the circularity: India buys record volumes of Russian crude, refines it at Jamnagar, Vadinar and elsewhere, and ships a slice of it back to Russia as finished gasoline, which Russia then subsidises on arrival. The self-styled energy superpower, run by hyper greedy siloviki, paying a premium to buy back its own molecules, cracked in Gujarat. That looks risky to me too.

Today, the Financial Times came out with a remarkable report [link]: an unprecedented wave of Ukrainian drone attacks on Russian shipping during July. According to the paper, Ukraine struck more than 110 Russian vessels in just nine days in the Sea of Azov, making it one of the most concentrated maritime attack campaigns ever recorded.

The objective is straightforward. Rather than chasing individual ships, Ukraine is systematically targeting the logistics chain sustaining Russian military operations in occupied southern Ukraine and Crimea. According to Tomas Alexa, senior analyst at maritime security firm Ambrey, even the Iran-Iraq Tanker War of the 1980s saw roughly 450 attacks spread over seven years. Ukraine has now exceeded a quarter of that total in little more than a week.

“I cannot stress enough how unprecedented this is,” Alexa told the Financial Times. “We have never seen anything so concentrated on a global scale.”

Ukraine’s Unmanned Systems Forces announced that a further eleven Russian vessels had been struck overnight, including five tankers, five cargo ships and a tugboat, bringing the reported total to 116 vessels in just nine days.

“The goal of the operation is to systematically disrupt the enemy’s logistics chain,” the force stated. “Disabling tankers, cargo ships and auxiliary vessels complicates the export of oil and petroleum products, limits maritime transport capabilities, and reduces the enemy’s ability to supply fuel to its forces and occupation grouping in temporarily occupied Crimea.”

This matters because it adds yet another friction to any future gasoline import program. Russia would not merely have to find the gasoline, the ships and the subsidies. It would also have to move those cargoes through an increasingly contested maritime environment.

So can India help? Absolutely. The economics mean that it almost certainly will, at the margin. But margins are exactly the point. India can shave the top off Russia’s gasoline deficit. It cannot eliminate it. Stack the constraints together: uncertain sanctions waivers, the legal grey zone surrounding import cargoes, punishing ton-miles, limited clean-product tanker availability, a shadow fleet already working close to capacity, subsidies required to make the economics work, and India’s own domestic market. None of those constraints is fatal on its own. Together they become formidable.

My base case is that Russia can probably sustain imports in the neighbourhood of 50kbpd, perhaps 100kbpd with determined political support and generous subsidies. Three hundred thousand barrels a day, the sort of volume required if Ukraine permanently disables another third of Russia’s gasoline production, looks far more like a strategic sealift than a commercial trade. At that point the question is no longer where the gasoline comes from. It is whether enough ships, terminals, rail capacity and willing counterparties exist to move it every single day for months, perhaps years.

Could that change? Of course. Sanctions evolve, fleets expand and traders invariably find creative ways to make money. But as matters stand today, imports are a painkiller, not a cure. The gasoline can be produced. The ability to deliver it into Russia, economically, reliably and at scale, is the real scarcity.

China To Rescue?

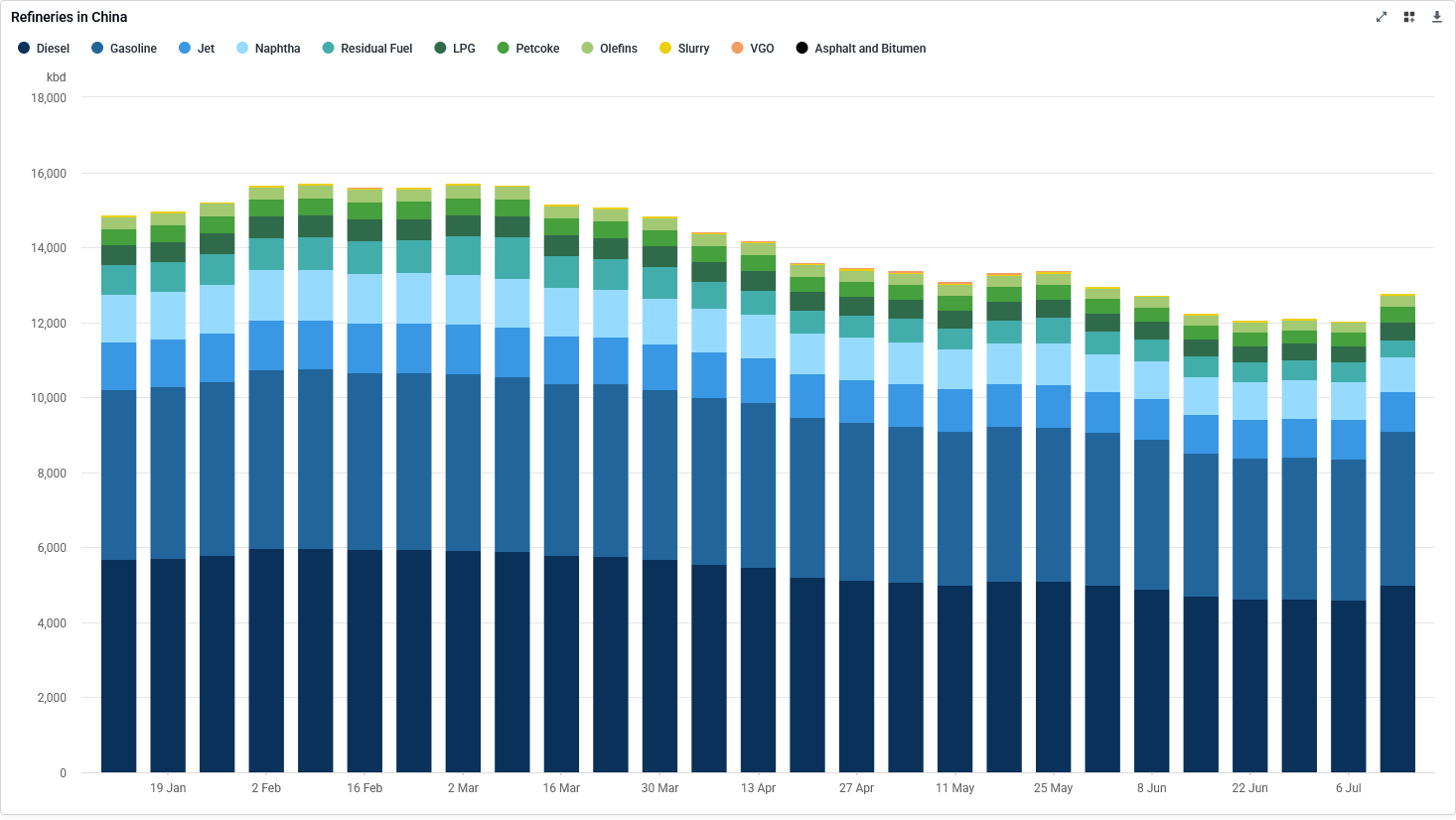

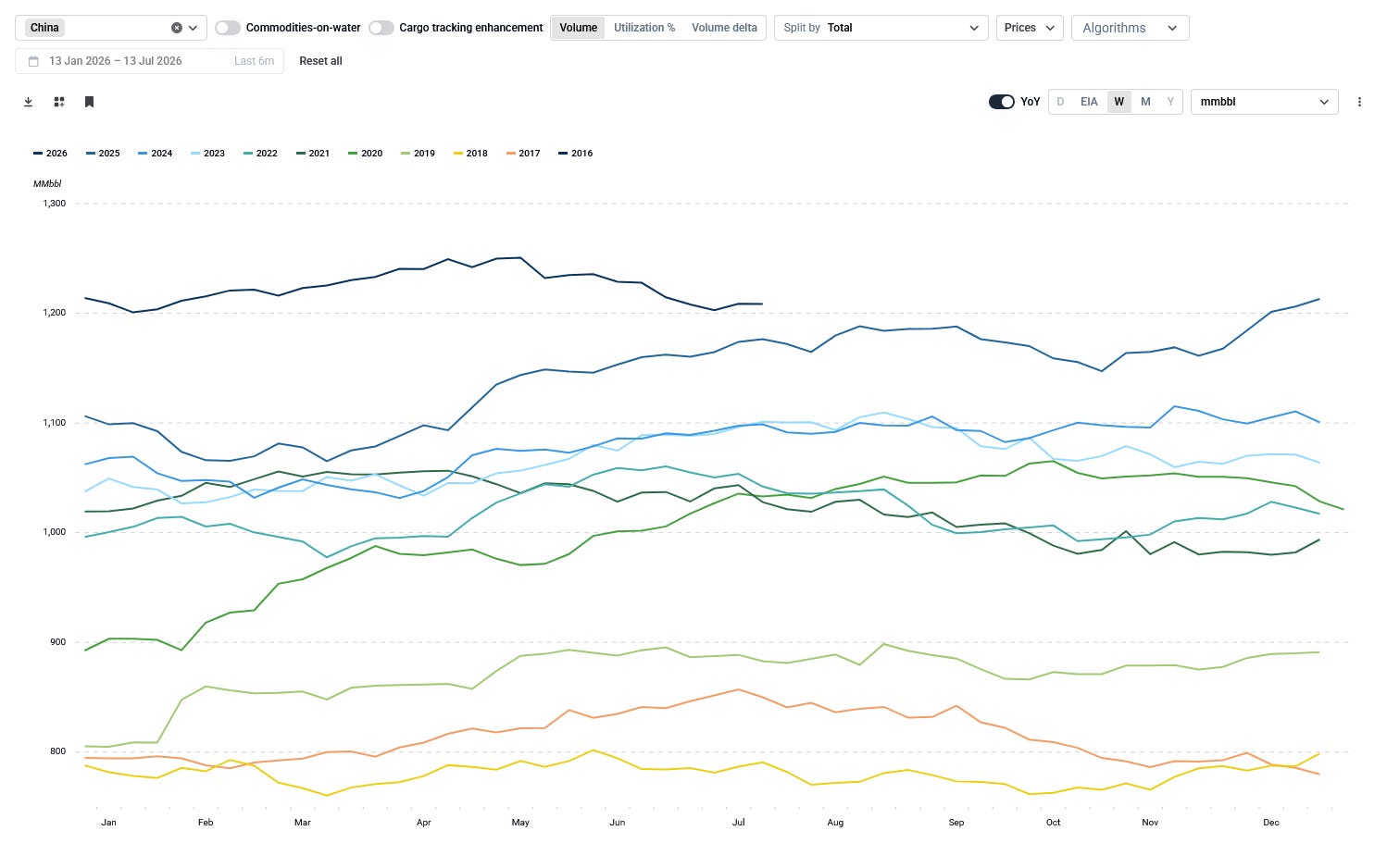

Which brings us to China, now the world’s largest refining system with roughly 17–18mbpd of installed capacity — about three times India’s and marginally larger than that of the United States. Actual refinery runs, however, currently tell a very different story.

At first glance, the set-up resembles India’s: domestic gasoline prices are materially higher than Russia’s, China imports large volumes of discounted Russian crude under its strategic partnership with Moscow, and plenty of idle refining capacity sits ready.

China is also the world’s only major importer of Iranian crude. The Trump administration temporarily relaxed sanctions during the Strait of Hormuz crisis, but withdrew that waiver this week after repeated Chinese breaches of the Memorandum of Understanding.

Unlike India, however, China remains trapped in a prolonged economic slowdown — for reasons I have discussed extensively on this Substack — and domestic fuel demand is exceptionally weak. That weakness forced Beijing into a remarkable balancing act during the Strait of Hormuz crisis. The objective was simple: keep domestic fuel markets fully supplied while avoiding any meaningful drawdown of strategic crude inventories.

The solution was extraordinary. China slashed seaborne crude imports from around 12mbpd to roughly 6mbpd, cut refinery runs from about 15mbpd to 12mbpd, shifted refinery yields towards gasoline at the expense of naphtha, maximised coal-to-gasoil production to offset the lower refinery output — and effectively suspended petroleum product exports, prioritising domestic consumption over export margins.

The consequence: crude inventories barely moved. The adjustment ran instead through petroleum product inventories — which, unhelpfully, cannot be monitored independently by satellite, since they sit largely in closed-roof tanks.

None of this was particularly profitable. Refinery margins were squeezed between government-controlled retail fuel prices and crude purchased at above US$100/bbl for almost four months. Then again, most of the large refiners are state-owned enterprises (SOEs) and profitability was never the priority for the CCP’s SOEs.

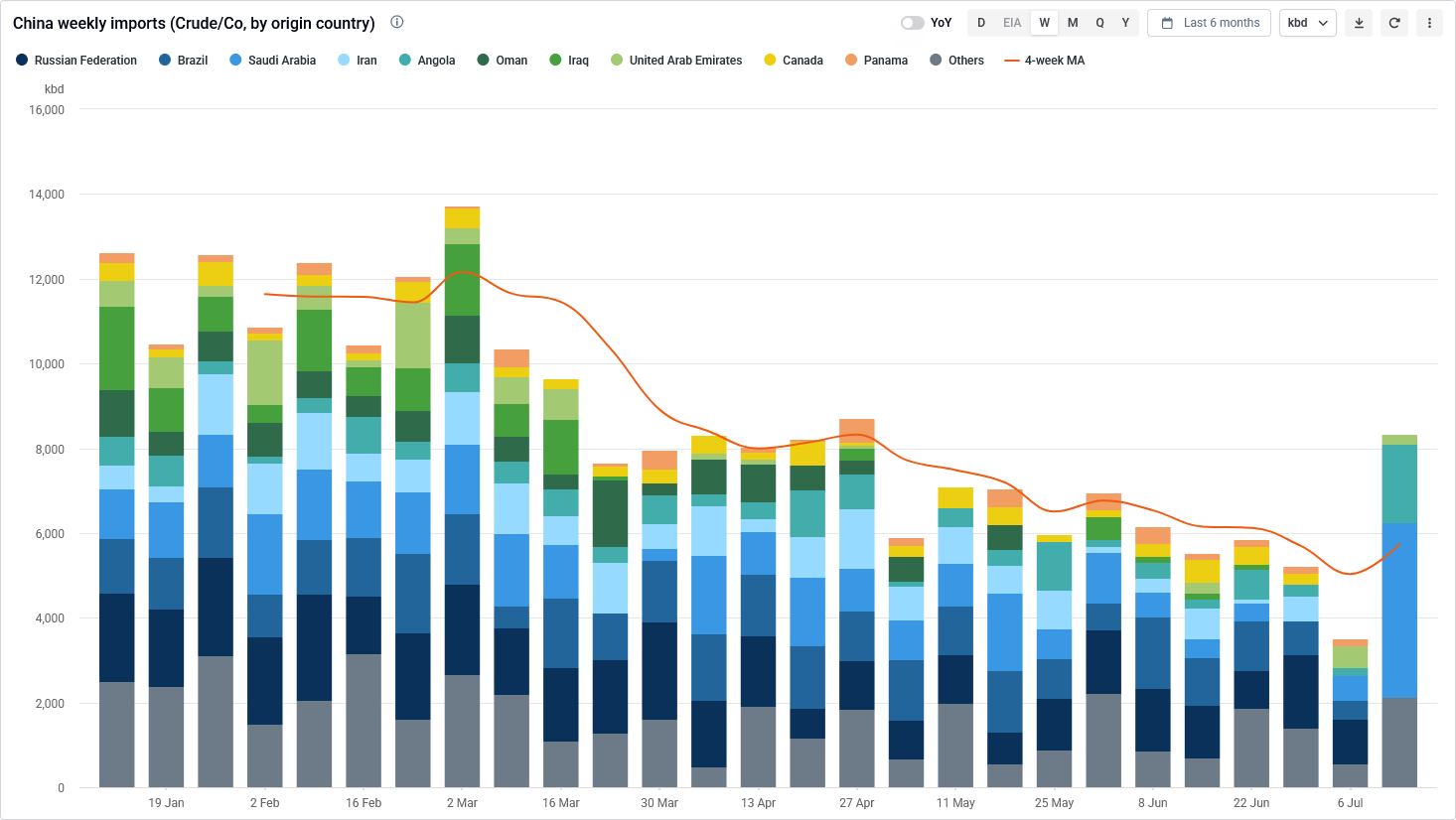

With crude prices retreating, China has lifted seaborne crude imports from roughly 6mbpd to around 8mbpd last week. Where this ultimately settles is too early to call. Beyond renewed Saudi volumes following the brief reopening of the Strait of Hormuz — note that the Strait is again functionally closed — much of the incremental crude remains unidentified in Kpler’s tracking system and is most likely discounted Iranian barrels.

Even so, I do not expect China to return to pre-war seaborne crude imports of roughly 12mbpd anytime soon - certainly not in 2026. The country has already likely achieved substantial fuel substitution with a workable equilibrium not to draw too much crude stocks.

Meanwhile, export quotas - a source of future higher runs - remain tightly controlled by Beijing. Yes, Bloomberg reports that authorities have approved around 1.3 million tonnes of product exports for July — roughly 335kbpd at a typical gasoline/diesel/jet split — to at least three refiners, including private processor Zhejiang Petroleum & Chemical and several state-owned names. But I read such articles as a distraction rather than a hint of where this is going. Let me explain.

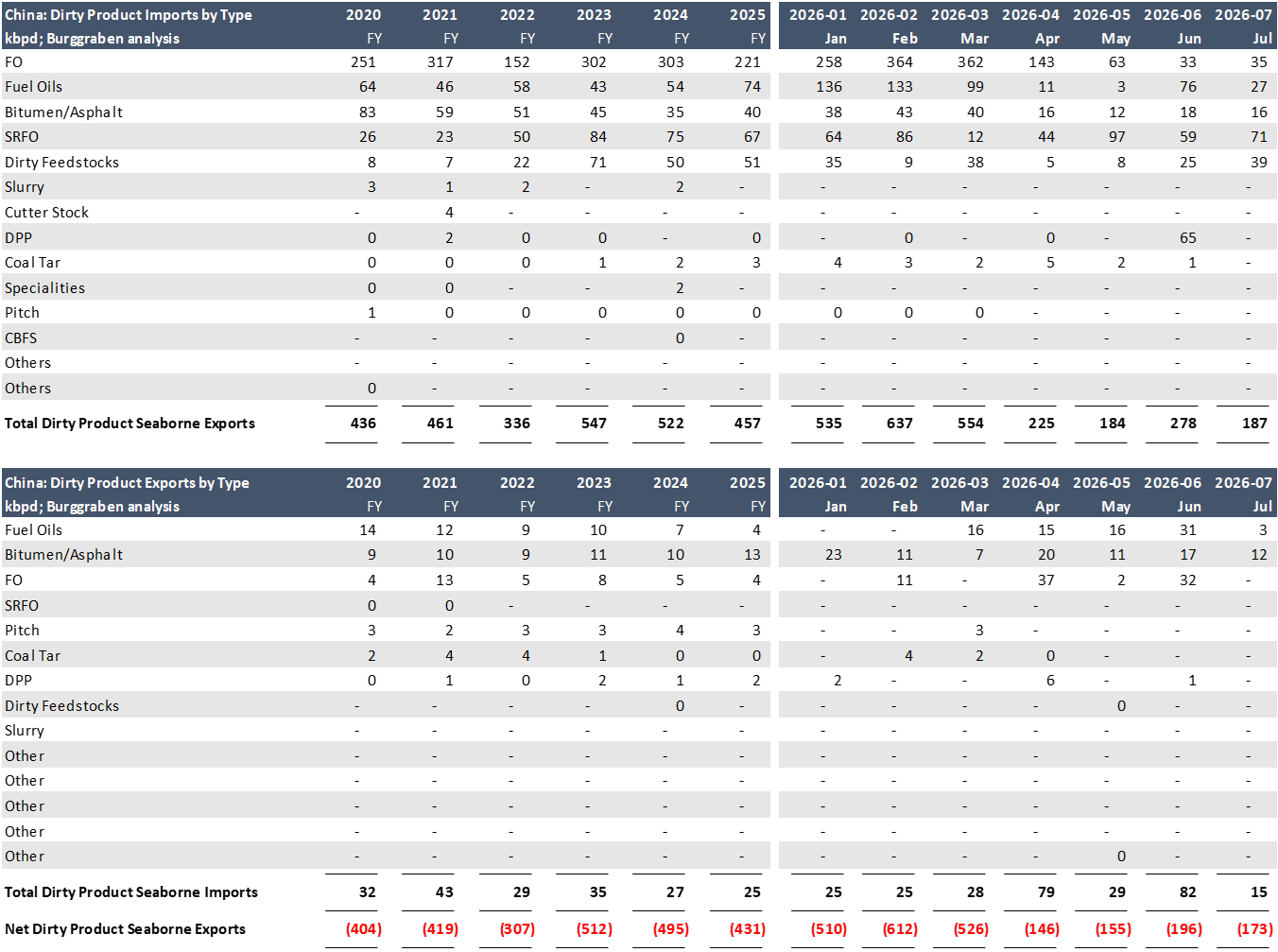

China isn’t the clean-product exporter Russia needs. Neither gasoline nor diesel nor jet was ever regularly on the export menu — and where it was, the volumes were symbolic. For years, China’s product trade was essentially naphtha, mainly with South Korea’s giant chemical industry, alongside other Asian buyers. Readers who have studied my China episodes on this Substack will recognise the pattern: this is about managing China’s own industrial overcapacity — in chemicals as much as anywhere — not about exporting petroleum products to optimise refinery margins.

Indeed, throughout this decade China has remained a net importer of both clean and dirty petroleum products. All of this suggests the CCP is managing its own energy independence, not the utilisation — and thus economics — of its refining SOEs. As David Baverez’s book argues, the CCP remains in the mindset of a “war economy”, and the only thing that truly matters to it is geopolitical independence.

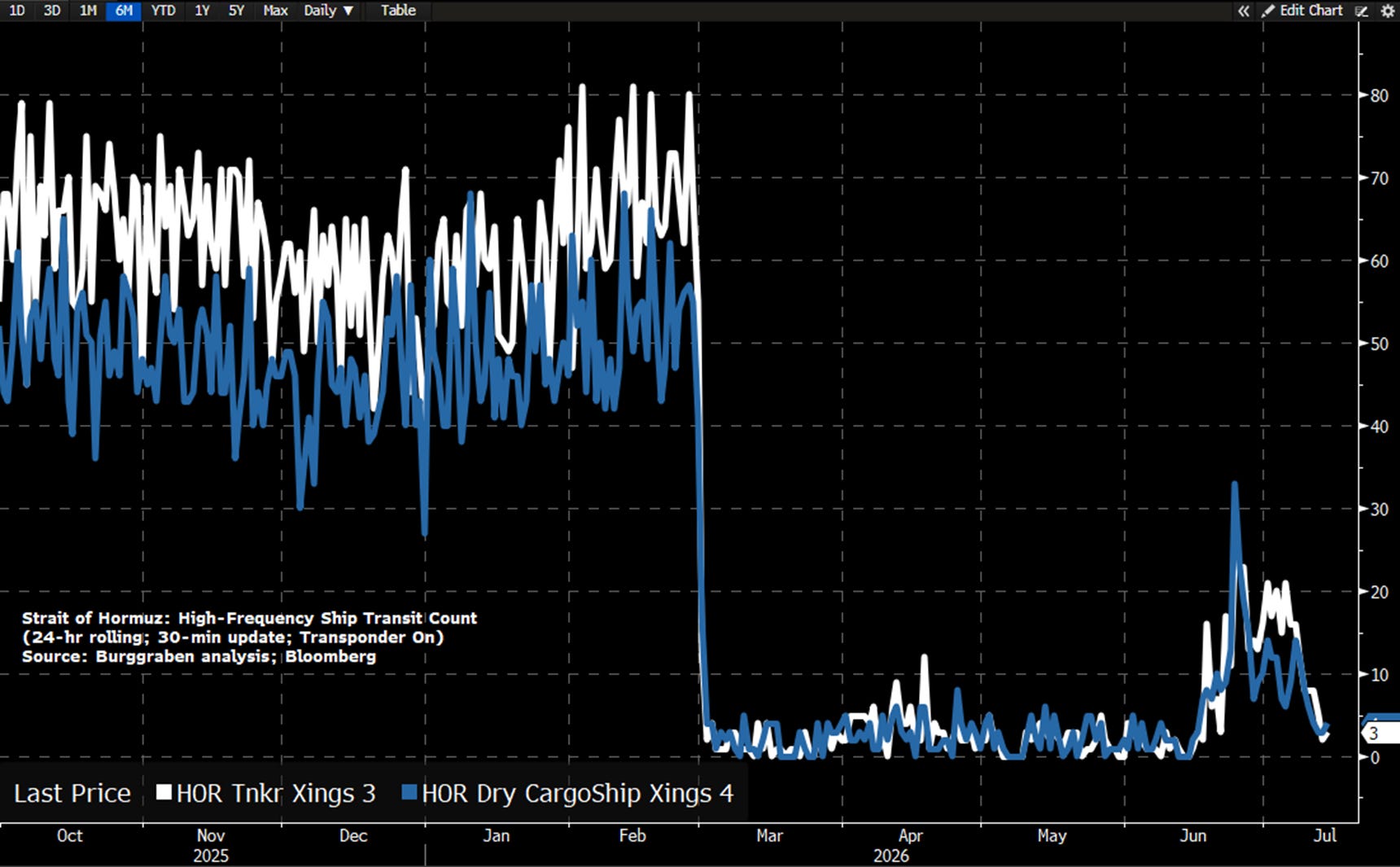

Moreover, refinery runs are unlikely to return to previous levels unless three conditions are met: the Strait functionally — and sustainably — reopens, export margins turn exceptional, and Beijing allows its refiners to chase them. None of these holds today. For the purpose of oil flows, consider the Strait of Hormuz closed again as of this week — not denying some dark-fleet shuttling, which by definition cannot be measured, only inferred in hindsight.

I have warned repeatedly here, here, here and here, and also in a recent interview (in German), that this administration cannot fix a “deal” with a terrorist regime — and that the Memorandum of Understanding was in truth a Memorandum of Misunderstanding. What do I mean by that?

The MoU is an exercise in constructive ambiguity — the Kissinger playbook of deliberately vague language so that both sides can claim victory. On the one hand, it assigns responsibility for reopening the Strait to Iran. It states that “the Islamic Republic of Iran will make arrangements using its best efforts for the safe passage of commercial vessels” and that Iran, in consultation with regional states, will determine the future administration and maritime services of the Strait. Tehran wanted that language because it provides a commercial escape hatch from sanctions while preserving its claim to control.

On the other hand, the MoU also demands that military obstacles be cleared and commercial traffic resume immediately. In practice, that means merchant vessels use the Omani shipping lane to escape the Persian trap. The consequence: Iran loses its de facto control over the Strait — something the regime appears to have realised over the past 24 hours. That is why it attacked a commercial vessel in the Omani lane: to reassert control. In doing so, it is now in breach of the MoU, prompting the US to retaliate — somewhat symbolically — with overnight strikes against Iranian military assets near the Strait.

But as I have said many times, neither side gives a fig about the MoU. Iran’s regime wants time — time to refinance itself and to preserve leverage through control of the Strait. Trump wants lower oil prices going into the midterms. Once that political objective is achieved, the odds of the shooting starting again are, in my view, materially higher.

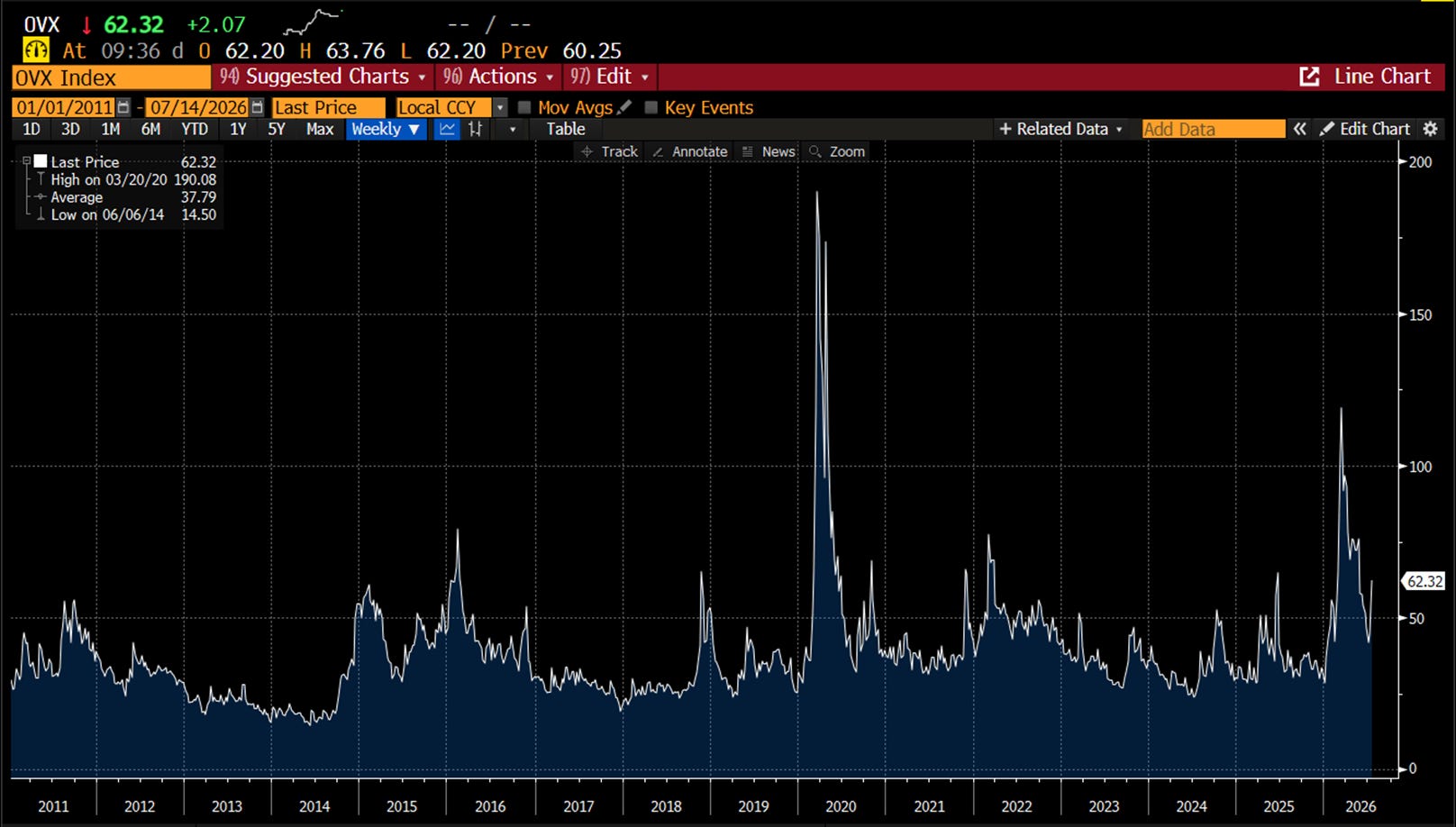

Either way, stable crude supply remains a prerequisite for the CCP to raise runs — and that condition remains absent. Brent is back at US$85/bbl, and OVX — oil’s implied volatility — is on the move again, now at 62 against a “stable” reading of 35 or below. The market continues to search for oil’s equilibrium price, and if you read my last Substack on the history of the oil price carefully, you will know it always will. We remain firmly in the Boom-Bust III era.

"But surely China has to help its ally Russia?" Not at all. Beijing has been consistent for years: China's own energy security comes first. Whenever geopolitical uncertainty rises, the CCP becomes more conservative, not less — the priority shifts towards protecting domestic supply, not maximising refinery utilisation or export profits. Time will tell. But from Russia's perspective, China is far from the obvious solution to its crisis.

The Near Abroad Won't Save Russia

Having ruled out most of the seaborne market, let us turn to Russia's immediate neighbourhood: Belarus first, then Kazakhstan. The rest of the former Soviet Union cannot help.

Belarus - the best Address but for How Long?

Belarus is, without question, Moscow’s best remaining option. It is also no more than that.

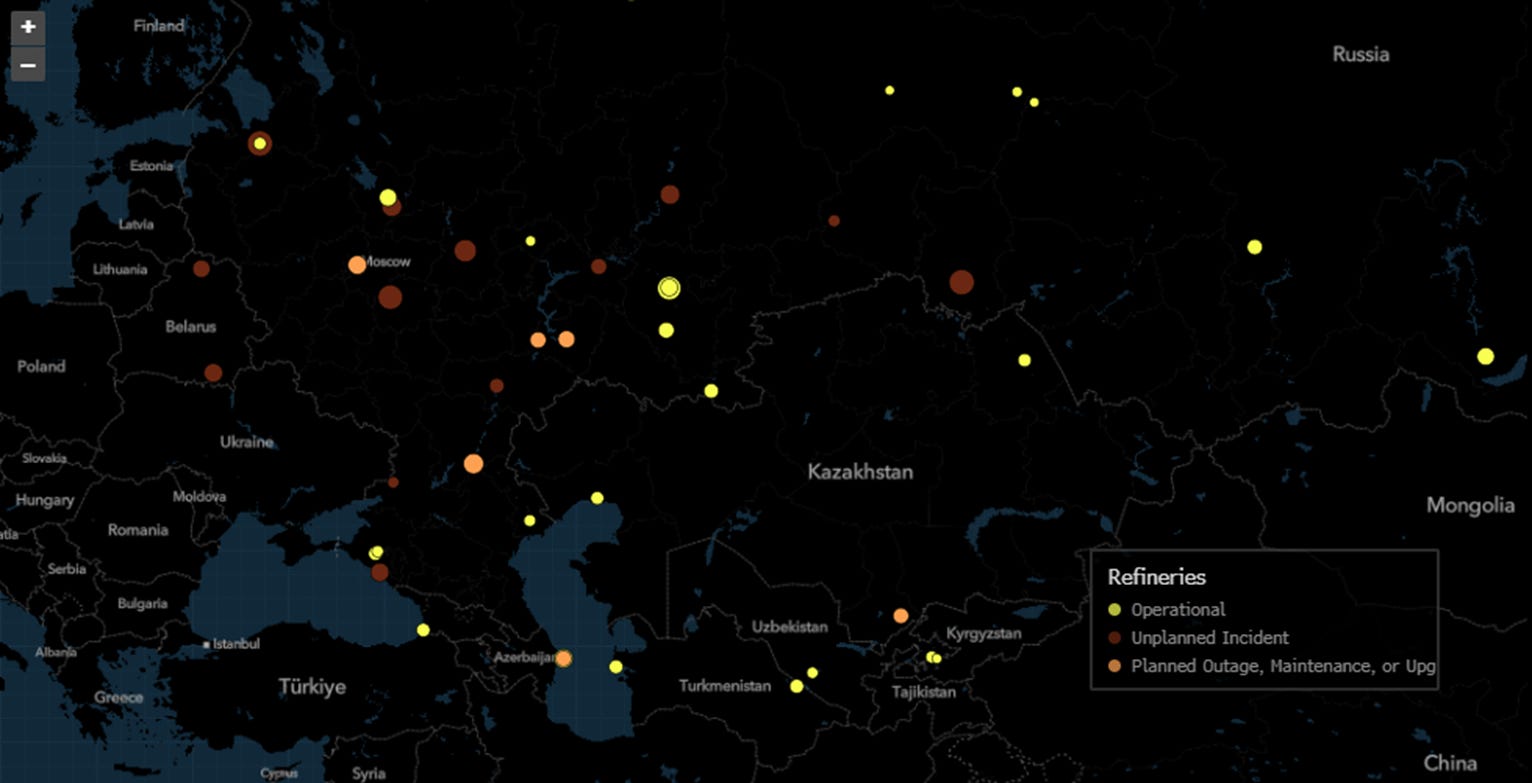

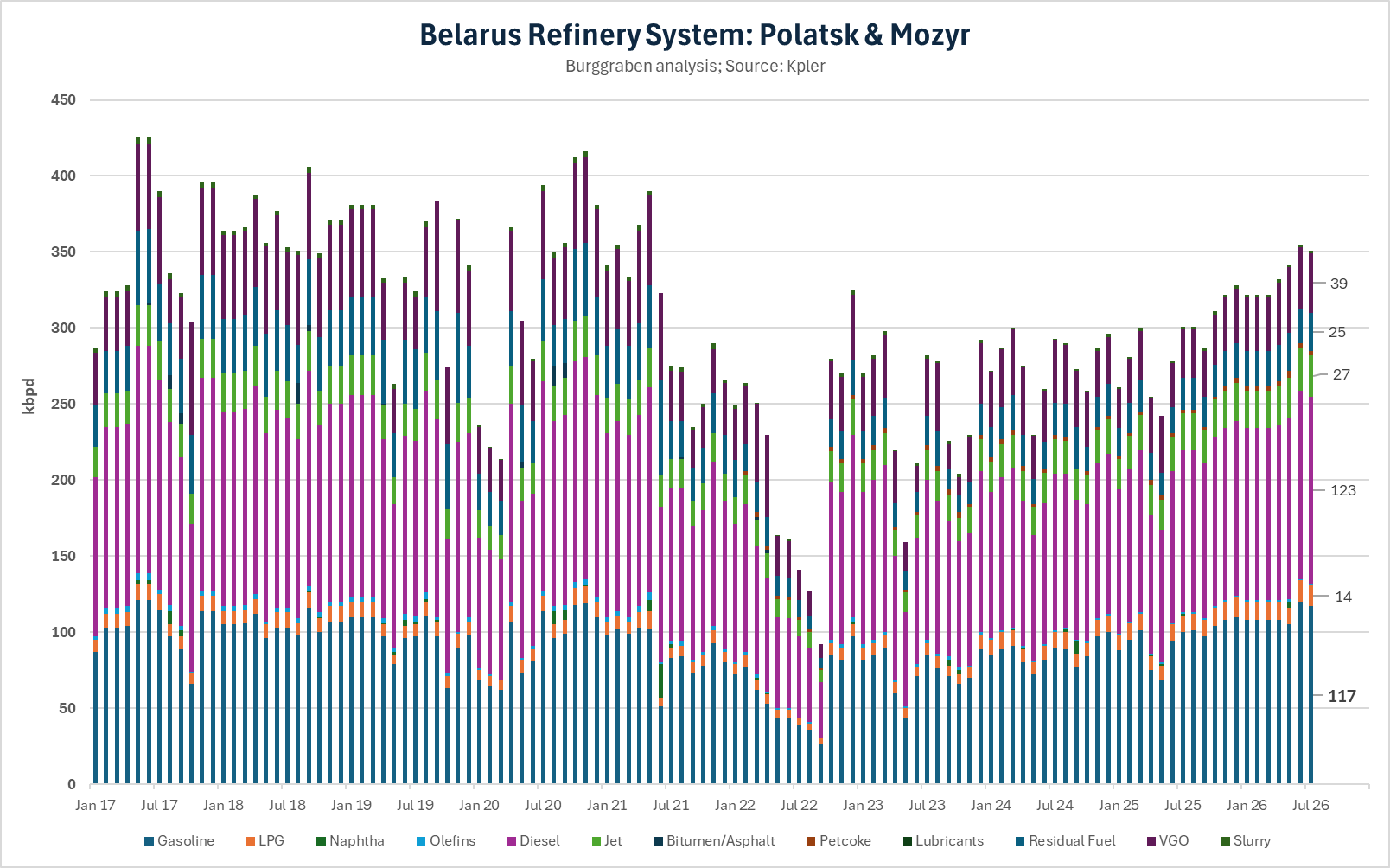

The country operates two modern refineries, Naftan in Novopolotsk and Mozyr, both ideally positioned to supply western Russia by rail with exactly the gasoline Russia is now short of. Despite what the Bloomberg map above may suggest, both refineries remain operational. Better still for Moscow, Belarusian pump prices sit broadly in line with Russia’s, eliminating the pricing problem that plagues almost every other potential supplier.

Naftan and Mozyr each process roughly 160-180kbpd and together run almost exclusively on Russian Urals delivered through Transneft’s Druzhba pipeline. That gives the Kremlin considerable leverage. There are few more uncomfortable positions in geopolitics than being indispensable to a regime that values power above everything else.

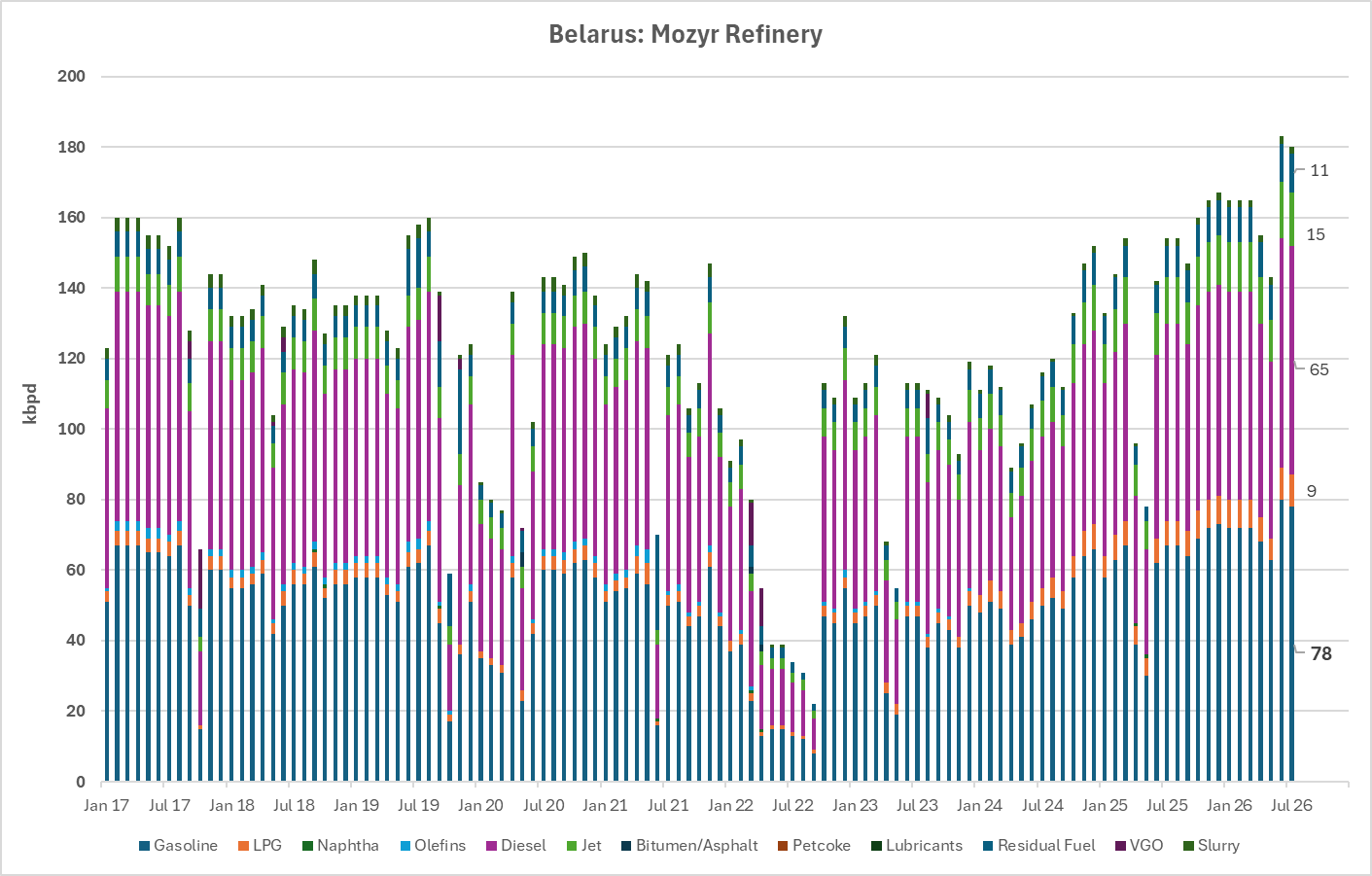

In June 2026 the two refineries produced roughly 117kbpd of gasoline against domestic Belarusian demand of just 24kbpd, theoretically leaving around 90kbpd available for export. Mozyr, in particular, has been pushed well beyond its 2024 operating levels and is effectively running flat out.

Given those numbers, there is little doubt what happened next. The Kremlin almost certainly instructed Lukashenko to divert as much gasoline and, increasingly, jet fuel as possible into Russia. The data suggest he is doing exactly that. According to Pavel Latushka [link], Belarusian gasoline shipments to Russia between 1 and 22 May increased fifty-eight-fold from a year earlier, while jet-fuel exports quadrupled.

The problem is that Kyiv understands those numbers just as well as Moscow. President Zelensky has already warned Lukashenko publicly that continued fuel deliveries make Belarus part of Russia’s military logistics chain. By our numbers, Lukashenko has ignored that warning so far.

That raises an uncomfortable question. How long does Mozyr remain off limits?

Unlike Omsk, which lies roughly 2,500 kilometres from Ukraine, Mozyr sits barely sixty kilometres from the Ukrainian border. It is effectively within Ukraine’s backyard. That makes it one of the easiest major refineries in the Russian supply chain to reach, whether by long-range drones or, if matters were ever to escalate dramatically, by other means.

I would therefore be cautious about treating Belarusian gasoline as a permanent solution. It may prove to be the next target instead.

All the Evidence Points to Kyiv

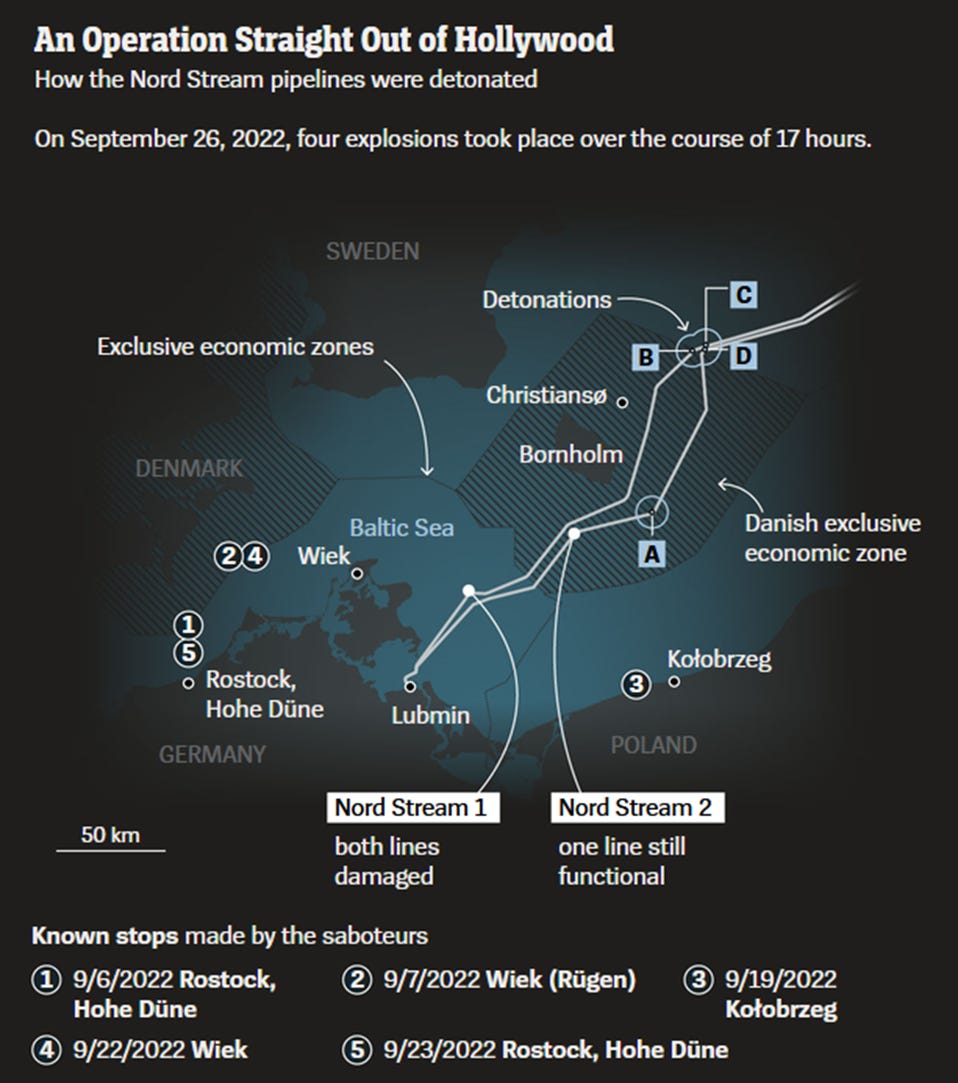

Der Spiegel‘s investigation into the Nord Stream sabotage, English edition, August 2023 (link)

The vessel was almost comically unremarkable. The Andromeda was a Bavaria 50 Cruiser — a production sailing yacht seafarers sneer at as the “Škoda of the seas” — and by 2022 a tired one: dented topsides, a 75-horsepower diesel that rattled like a farm tractor, a broken autopilot, a head that stank. In early September a crew of six — five men and a woman, travelling on forged papers, among them a doctored Romanian passport — chartered her from a small rental outfit in the Warnemünde marina at Rostock. No other sailor on the Baltic gave her a second glance. That was the point.

Over the following weeks the Andromeda wandered the southern Baltic — a stop at Wiek, where the harbourmaster obligingly topped up her fuel tank, a quiet detour south to the Polish resort of Kołobrzeg, and back to Rostock by 23 September, three days before the seabed shook. On the night of 26 September 2022, divers from that unremarkable little yacht went down and blew holes in three of the four steel pipes of Nord Stream 1 and 2. It was the largest act of infrastructure sabotage in modern European history — in the words of Germany’s own federal prosecutors, an attack on “the internal security of the state.” Forensics teams would later find traces of the very explosive used, aboard the boat.

A year on, after investigators from a dozen countries had chased every thread — the yacht, the DNA, the forged passports — Der Spiegel weighed the trail and concluded, flatly, that “all the evidence points to Kyiv.” And here is the tell that matters more than any single clue: nobody wanted to say so. Sweden and Denmark quietly wound up their inquiries without naming a soul; Germany locked its findings away on orders from the Chancellery. Because the answer was radioactive. Had it been Russia, Article 5 of the NATO treaty was in play. Had it been Ukraine, German public support for Kyiv might have collapsed overnight. Silence was the safest option for everyone.

For a year the comfortable assumption had been that reaching a pipeline on the deep Baltic seabed demanded a state’s toolkit — a submarine, naval mines, specialist deep-sea equipment — the sort of thing a country like Ukraine supposedly could not muster. That assumption is precisely why so many casual observers rushed to insist it must have been the Americans, sabotaging the pipeline to sell Europe more of their own LNG.

It was conspiracy rubbish, peddled by armchair commentators who had never served — anyone who had would have known you do not need a submarine to reach seventy-odd metres of water. Any offshore diving professional could have told them the same in a minute: commercial divers work far deeper than that every day, installing and maintaining oil-and-gas equipment. And the motive never held up anyway — America’s LNG is sold by private exporters, not the White House, and Biden would go on to freeze new export approvals altogether.

The truth was cheaper, and entirely of a piece with today’s assault on Russia’s refineries: a handful of divers and a rented yacht. No superpower required. The mission then was the mission now — cut the income to the Russian war machine. Occam's razor.

Kazakhstan - A Distraction

That leaves Kazakhstan.

At first glance, it looks promising. It is a major oil producer, a former Soviet republic and one of Russia’s closest neighbours. Look more closely and the case quickly falls apart.

The Soviet past does not make Kazakhstan an ally. Since independence, the world’s largest landlocked country has spent more than three decades rebuilding its language, national identity and statehood, fully aware that Russian nationalists, Vladimir Putin among them, have openly questioned whether Kazakhstan should exist as an independent country at all.

Its foreign policy is deliberately “multi-vector”: maintaining commercial ties with Europe, China and Russia alike while becoming strategically dependent on none of them. President Tokayev demonstrated that approach publicly in 2022 when, sitting beside Putin at the St Petersburg Economic Forum, he refused to recognise the so-called Donetsk and Luhansk People’s Republics. Since then, Astana has quietly complied with Western sanctions while carefully avoiding direct confrontation with Moscow. It has played the hand exceptionally well.

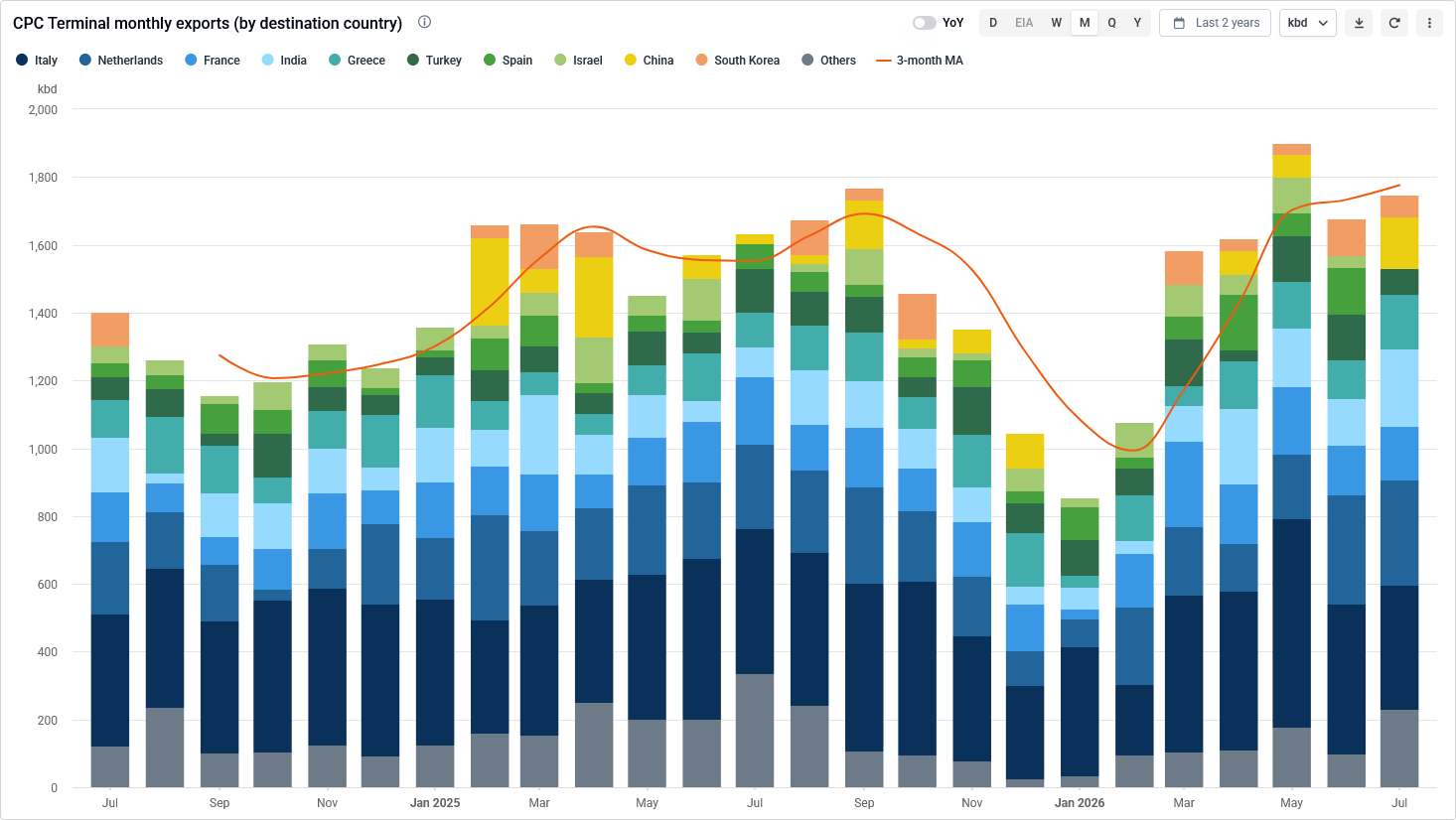

Kazakhstan imports no crude oil from Russia. None.

It produces and exports its own. The CPC Terminal alone shipped roughly 1.9mbpd during May 2026, while Kazakhstan’s refineries run almost entirely on domestic production. The Kremlin therefore holds virtually no leverage over Kazakhstan’s fuel system.

It does retain some influence over crude exports. The CPC pipeline crosses Russian territory before loading at Novorossiysk on the Black Sea.

But that leverage cuts both ways. Disrupting CPC would hurt Kazakhstan. It would also immediately hit Italy, which alone imports around 600kbpd through the system, alongside the Netherlands, France, Greece, Turkey and increasingly China.

Moscow would simultaneously antagonise Europe, Turkey and Beijing over export volumes it can ill afford to politicise. In my view, CPC keeps Astana polite. It does not make it obedient.

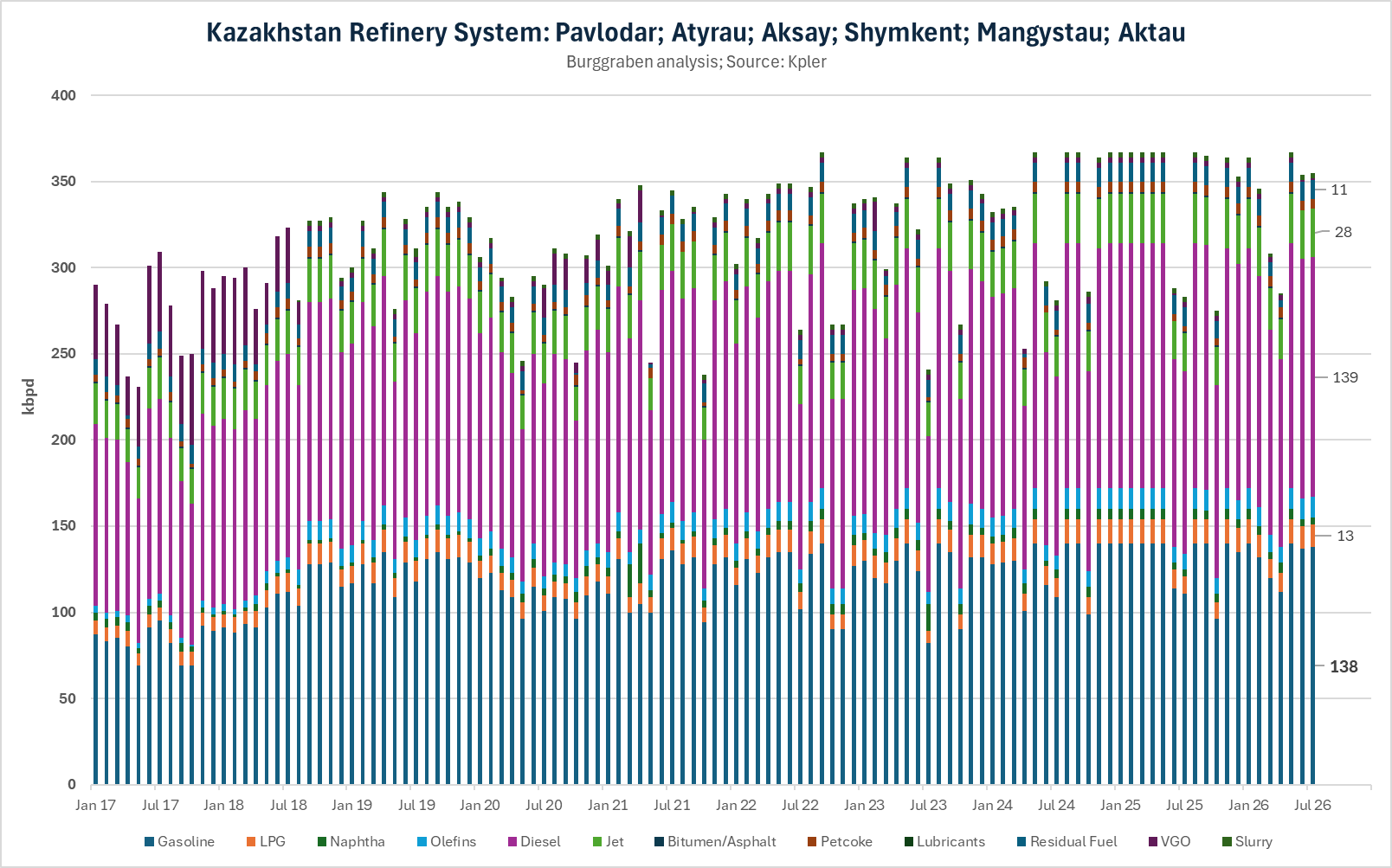

Could Kazakhstan at least export gasoline? Not in any meaningful quantity.

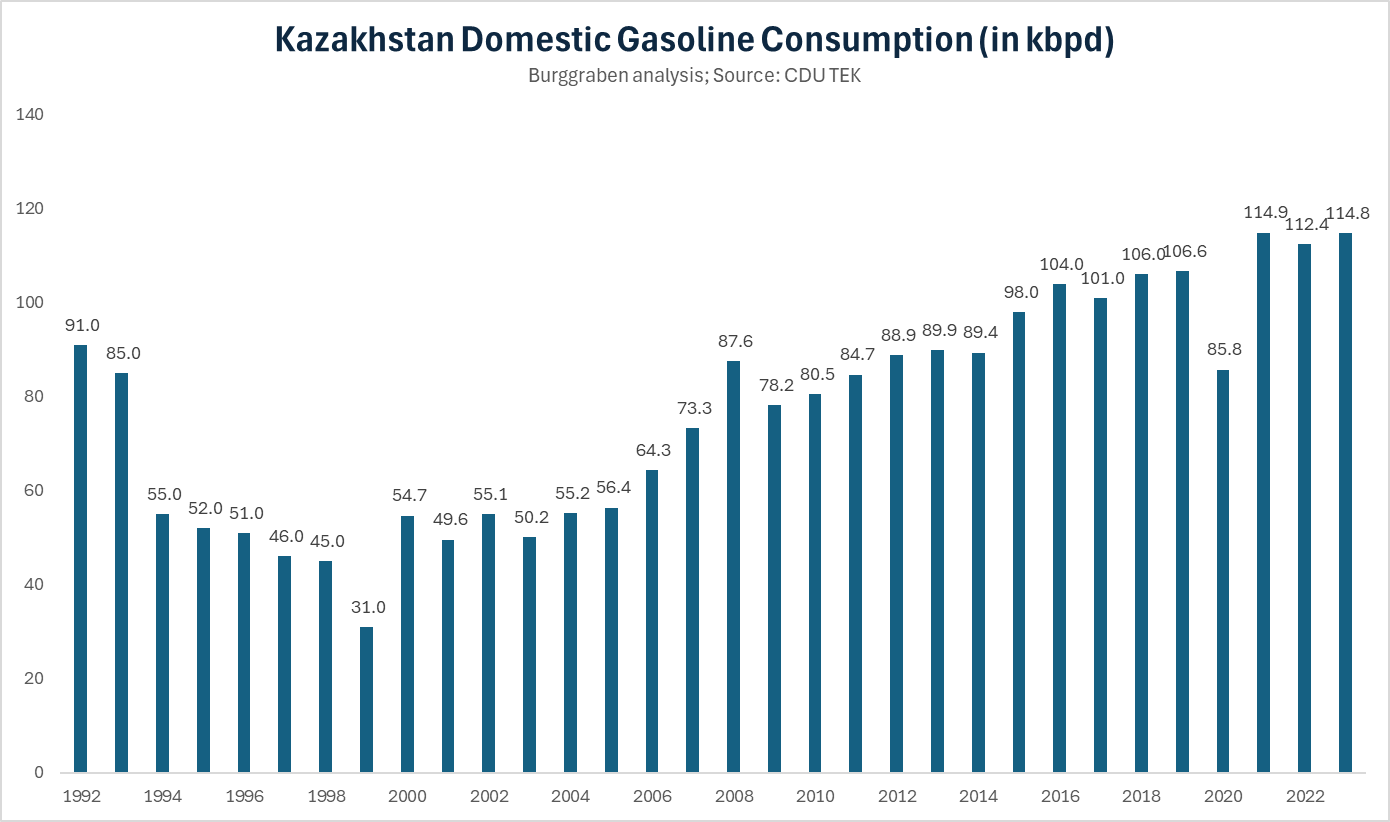

Its four refineries, Pavlodar, Atyrau, Shymkent and Aktau, produce roughly 138kbpd of gasoline against domestic demand of around 115-125kbpd. That leaves little more than the occasional cargo available for export.

Accordingly, Kazakhstan’s Deputy Energy Minister recently dismissed reports that Astana could provide Russia with 50,000 tonnes of gasoline as humanitarian assistance, calling the reports “unfounded” [link].

“We have received no official request from Russia,” he said. “Our priority is supplying Kazakhstan’s domestic market. If surplus volumes exist and there is a commercial opportunity, we will consider it.”

That statement reveals far more than it first appears. Kazakhstan’s principal concern today is not helping Russia. It is stopping Russians from buying Kazakh fuel.

According to local media [link], authorities have established new police checkpoints along almost sixty roads leading into Russia to combat so-called “gasoline tourism”. Border controls have been tightened, while vehicles are now generally limited to a single crossing each day.

That rather sums it up. Russia, the world’s second-largest crude exporter, is increasingly relying on neighbours whose immediate priority is preventing Russians from crossing the border to fill their tanks.

Kazakhstan is not Russia’s solution. It is another reminder of how few solutions remain.

Three Doors, None of Them Good

According to Mikhail Khodorkovsky, the Kremlin has only two “doors” out of the fuel crisis.

The first is the market solution: free gasoline prices and let them rise until demand falls back into line with supply. The second is the administrative solution: coordinate the railways, strategic reserves and oil companies well enough to move fuel across eleven time zones to where it is needed.

The Kremlin has chosen neither. Instead, it has reached for a third option that Khodorkovsky merely hints at: quietly lowering fuel standards and transferring the cost of the crisis onto ordinary Russians - Kremlin style.

Take them in turn.

The market solution is economically straightforward. Let prices find their equilibrium. In a dozen or so regions, gasoline might climb towards US$5 per gallon equivalent, demand would fall, fuel would flow to where it pays best, and within a few months the shortages would largely disappear. Economically, it works. Politically, it is impossible. The Kremlin cannot afford nationwide headlines showing Russians paying European fuel prices while fighting what it insists is a successful war.

Yet, in practice, Russia is already running exactly that experiment, albeit unofficially.

The only question is where the market clears. Judging by numerous reports on social media, somewhere around RUB170-250 per litre, roughly US$2-3. That would barely raise an eyebrow in much of Europe. In Russia, it is politically explosive.

Two recent examples illustrate the point. In occupied Simferopol, one driver finally found gasoline after fourteen days of empty pumps. The price was RUB249 per litre, purchases were limited to twenty litres and, tellingly, there was no queue [link]. The market had cleared. Near Novosibirsk, filling station owner Nikolai Fedotov simply posted RUB170 per litre and challenged anyone to complain. His land, his fuel, his price. If customers did not like it, they were free to drive elsewhere (link).

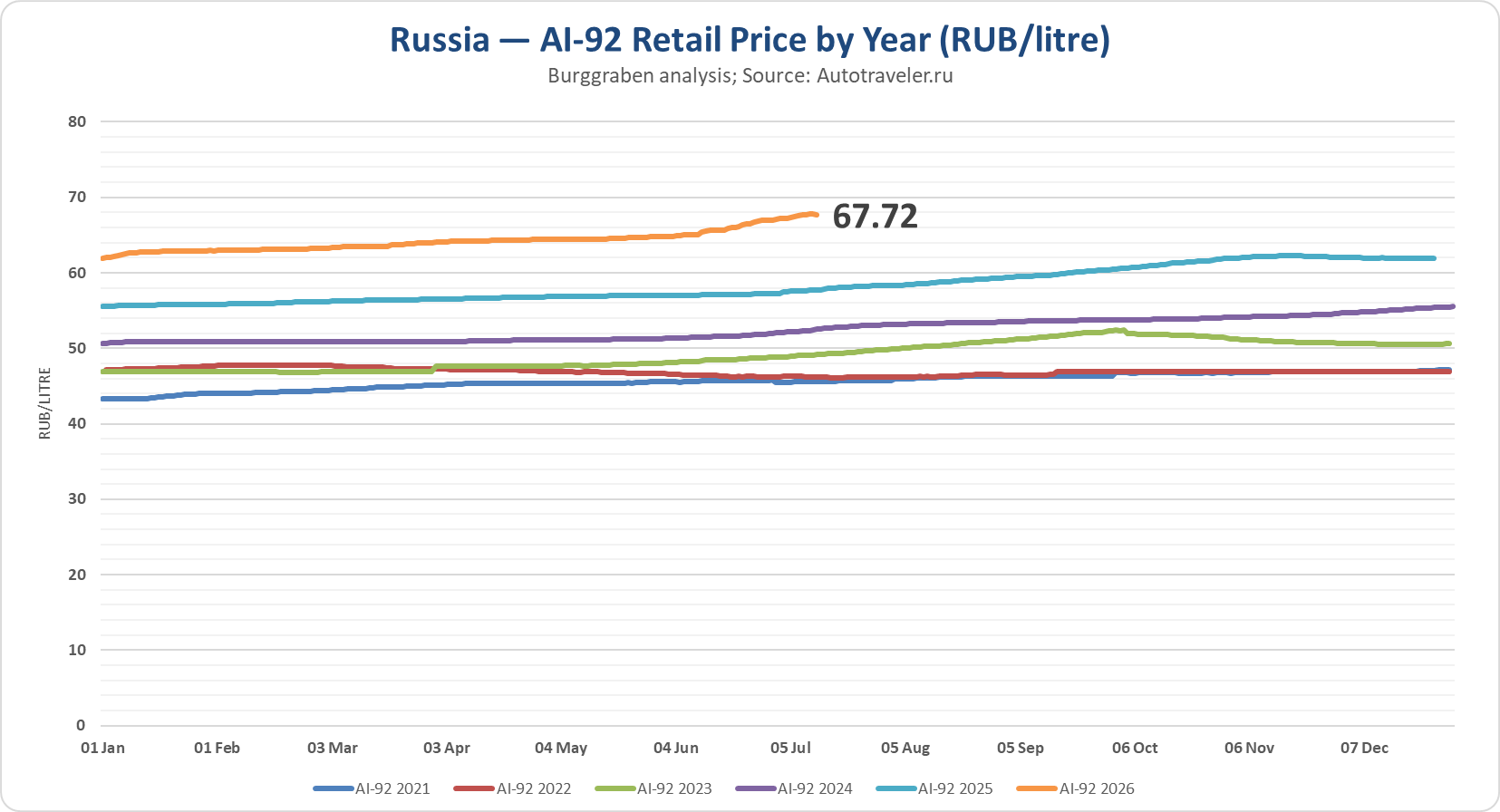

Which is why official prices remain anchored far below market-clearing levels. AI-92, the country’s benchmark gasoline grade, sells at an average of just RUB67.72 (US$0.88) per litre at most filling stations. The gap between the official and the market price is exactly where shortages, queues and corruption begin.

That is precisely why the Kremlin never officially opens the first door. It does not need to. This is Russia. Prices float anyway, not through legislation but through corruption. The Anti-Monopoly Service announces an investigation, a few envelopes quietly change hands and the investigation disappears. Multiply that across thousands of filling stations and you have de facto price liberalisation. Officially, prices remain controlled. In practice, they float on bribes. Corruption is not a side effect of the pricing mechanism. It is the pricing mechanism.

The second option is the administrative solution. On paper, it sounds perfectly reasonable. The state simply instructs companies to coordinate rail capacity, release strategic reserves and move fuel from surplus regions to deficit regions. That assumes a government capable of managing a continental logistics network under wartime conditions. If Russia still had such a government, it would not be in this crisis.

In All the Kremlin’s Men, Mikhail Zygar describes today’s Russian state not as an administration but as a medieval court, rewarding loyalty and proximity to power rather than competence. That system works remarkably well when distributing patronage. It performs rather less impressively when coordinating rail tankers across eleven time zones.

The oil industry itself illustrates the point. Khodorkovsky was imprisoned. Vladimir Yevtushenkov was placed under house arrest before losing Bashneft. Lukoil chairman Ravil Maganov died after falling from a hospital window. One by one, capable managers disappeared while their assets were consolidated under Igor Sechin’s Rosneft. A corrupt state can seize an oil company. That does not mean it can run one efficiently.

Catherine Belton reaches much the same conclusion in Putin’s People. The system built by the siloviki was never designed to administer efficiently. It was designed to extract wealth. Its organising principle resembled the obschak, the common cash pool of organised crime, where loyalty determined access to resources and the distinction between public and private wealth deliberately disappeared. That is the machine now expected to solve Russia’s fuel crisis. It was built to siphon. Not to supply.

Which leaves the third option. Quietly lower fuel quality and let motorists absorb the consequences.

Take Galina from Krasnoyarsk. One morning she stopped at a Gazprom filling station on her way to work and, delighted to find fuel available with hardly any queue, filled thirty litres of AI-92. Eight hundred metres later her engine died.

She was not alone. Roughly twenty-five vehicles reportedly broke down after refuelling at the same station. Some failed before leaving the forecourt. Others managed a few hundred metres. Drivers filmed visibly contaminated fuel flowing from the pumps. Rust, debris and other contaminants clogged injectors and damaged fuel systems. After cleaning, the cars ran normally again. The filling station continued operating. Gazprom had little to say.

This is what the Kremlin’s third option looks like in practice. It has not solved the fuel shortage. It has merely transferred part of its cost onto ordinary motorists.

Every crisis eventually reveals what a political system was built to do. Russia’s was built to extract, not to govern. Faced with a fuel shortage, it does not create more fuel. It raises prices unofficially, rewards corruption, lowers quality standards and asks ordinary Russians to pay the bill. That is not a temporary response to this crisis. It is how the system functions.