A Crude Awakening: Executive Summary

Why re-opening the Strait is unavoidable and will take time. A multi-episode deep dive into oil balances, crude quality, vessel traffic, demand destruction and the high-stakes game of geopolitics.

Executive Summary

Freedom of Navigation At Stake

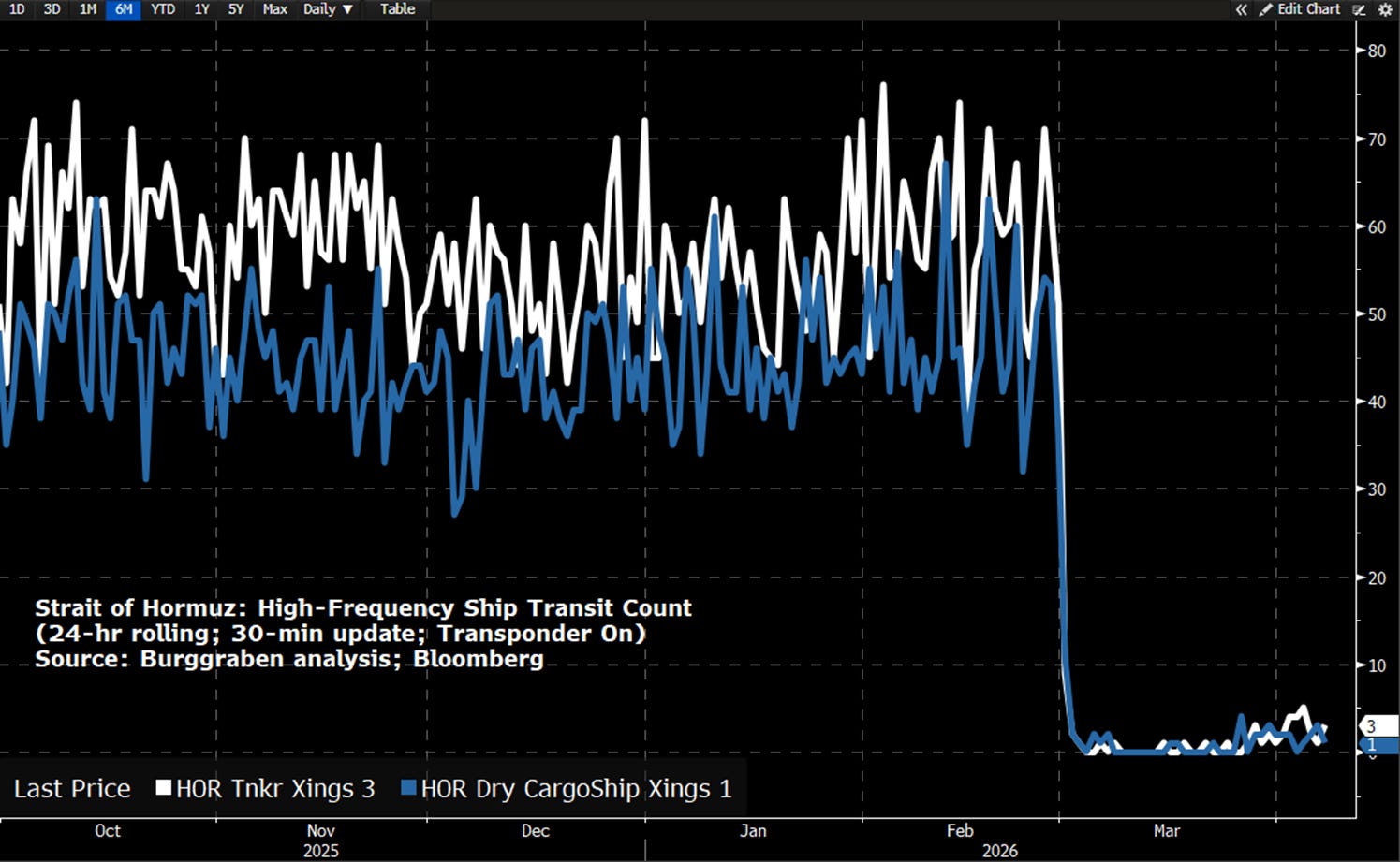

Iran did not need to sink a single tanker to shut down a fifth of the world’s oil and gas supply. A handful of missile and drone strikes was enough to deter the global commercial shipping industry from transiting the Strait of Hormuz.

Within two days, the vital energy chokepoint was functionally closed for exports. Only Iranian oil and gas continues to move through the Strait, with the odd exception that proves the rule and carries no relevance for the functioning of the world economy.

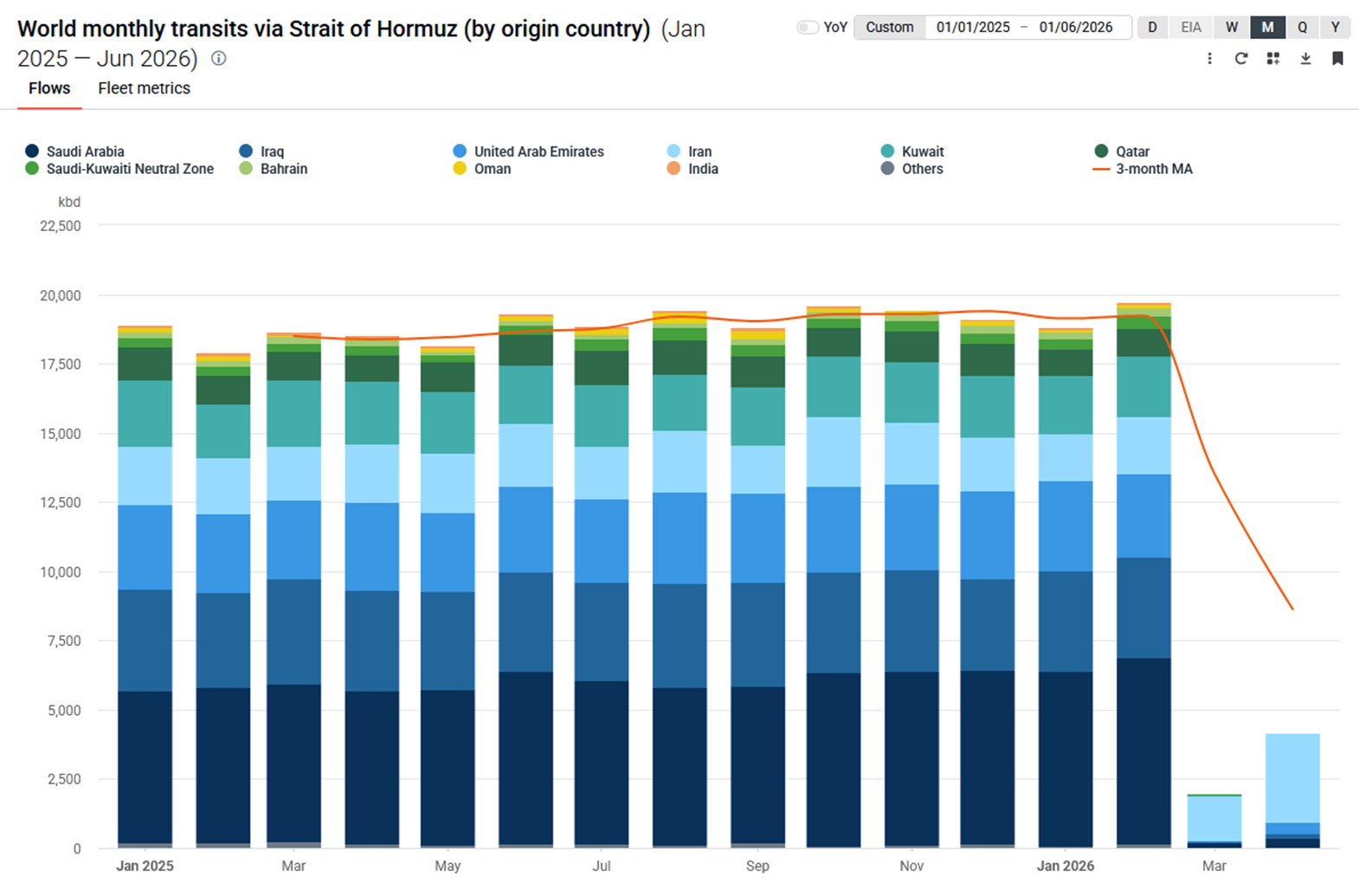

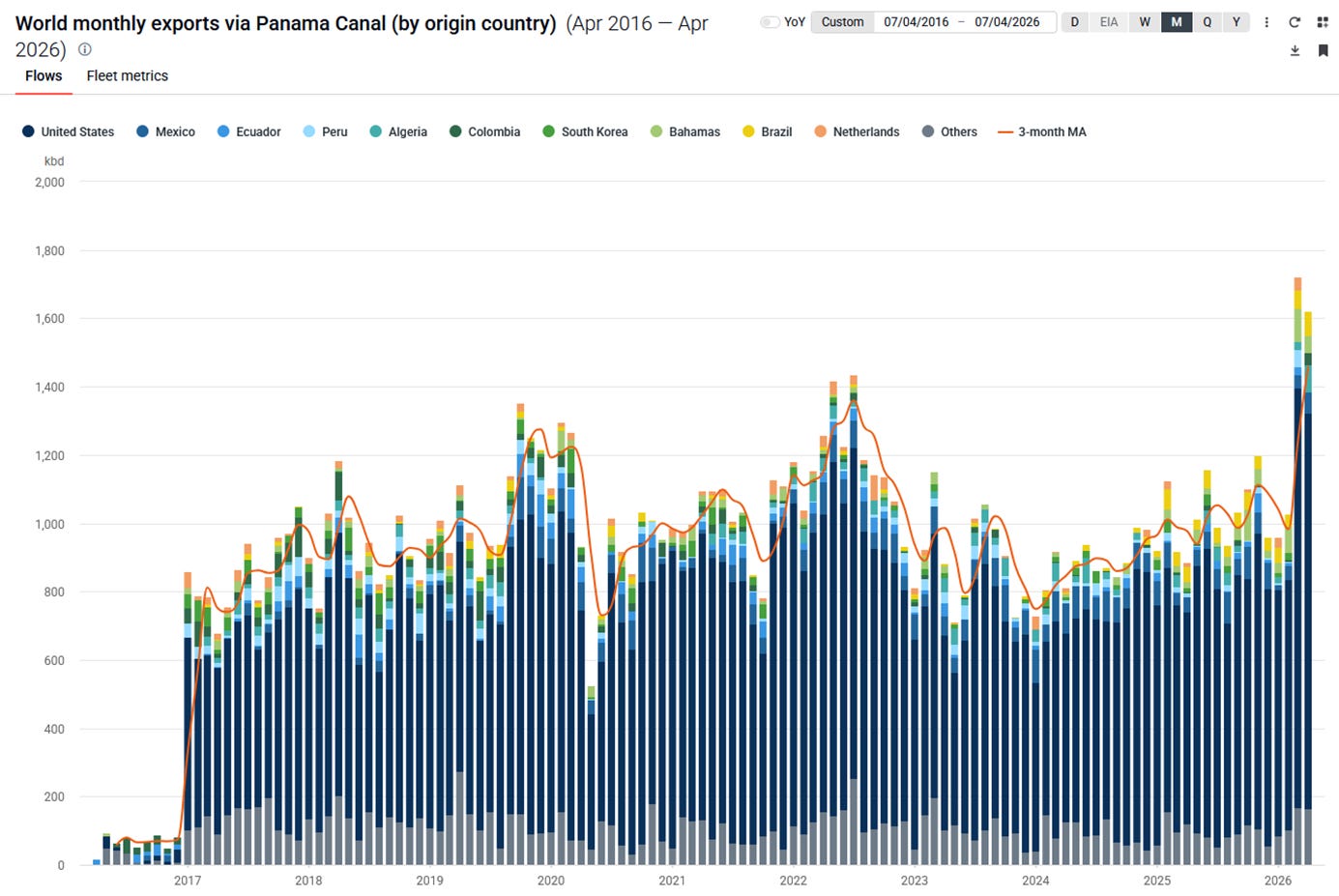

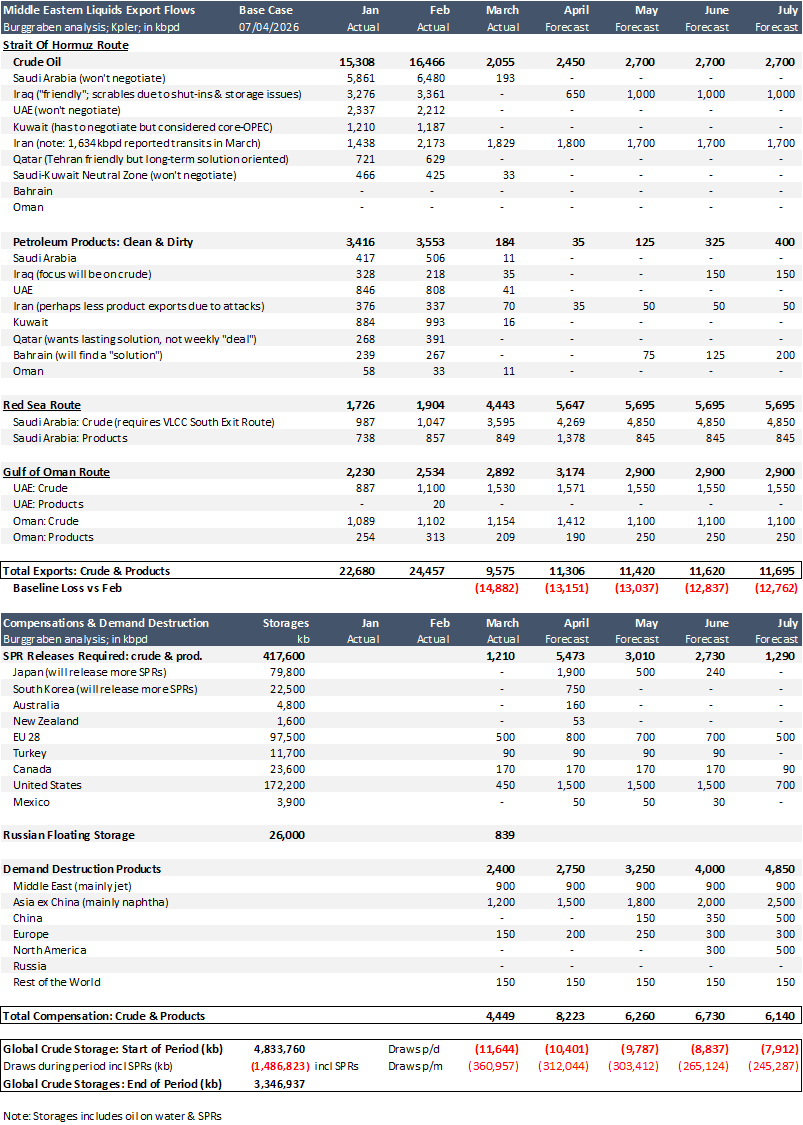

The most honest gauge of the current balance of power in this conflict is the chart below: monthly transits of oil and petroleum products through the Strait of Hormuz. Iran’s regime, not the United States, is in control of this war, as the only objective that matters now is regaining control of the Strait.

If that fails for a prolonged period, everybody outside Tehran loses. Everybody, including the United States and China. Every other 3D chess, game theory narrative, usually advanced by generalists with little understanding of oil, is not worth the paper it is written on.

Tehran’s strategy is one of economic attrition, built on the assumption that the United States cannot tolerate a prolonged war and elevated oil prices indefinitely and will eventually back down. If and when it does, Iran’s Revolutionary Guards will control Hormuz. Oil will flow again, but only on Tehran’s terms and at the right price.

This is a replicable playbook in an age of cheap but effective weapons proliferation. Interrupting freedom of maritime navigation is astonishingly simple. The reason is behavioural. The adversary is not a navy, it is a commercial vessel owner and an unarmed crew. Deterrence is as simple as stopping a car on the street with a gun in your hand. Often, an explicit threat is enough. Remember Captain Phillips? A true story.

Nor are such attempts rare in post-war history. There have been thousands of naval interventions by the United States, Britain and France, and increasingly by India and China, in response to disruptions, from the 1980s tanker wars in Hormuz to piracy off Somalia and in the Strait of Malacca. Maritime trade has always required policing.

If word spreads that this policing breaks down systematically, global commerce will suffer immeasurably, and with it the petrodollar system.

There are some 200 straits globally, with at least two dozen highly relevant for global commerce. Because they often overlap with territorial waters under the 12 nautical mile rule, they fall under the U.N. Convention on the Law of the Sea (UNCLOS) transit passage regime, which guarantees continuous, uninterrupted freedom of navigation for commercial and military ships and aircraft. The question is, who guarantees what?

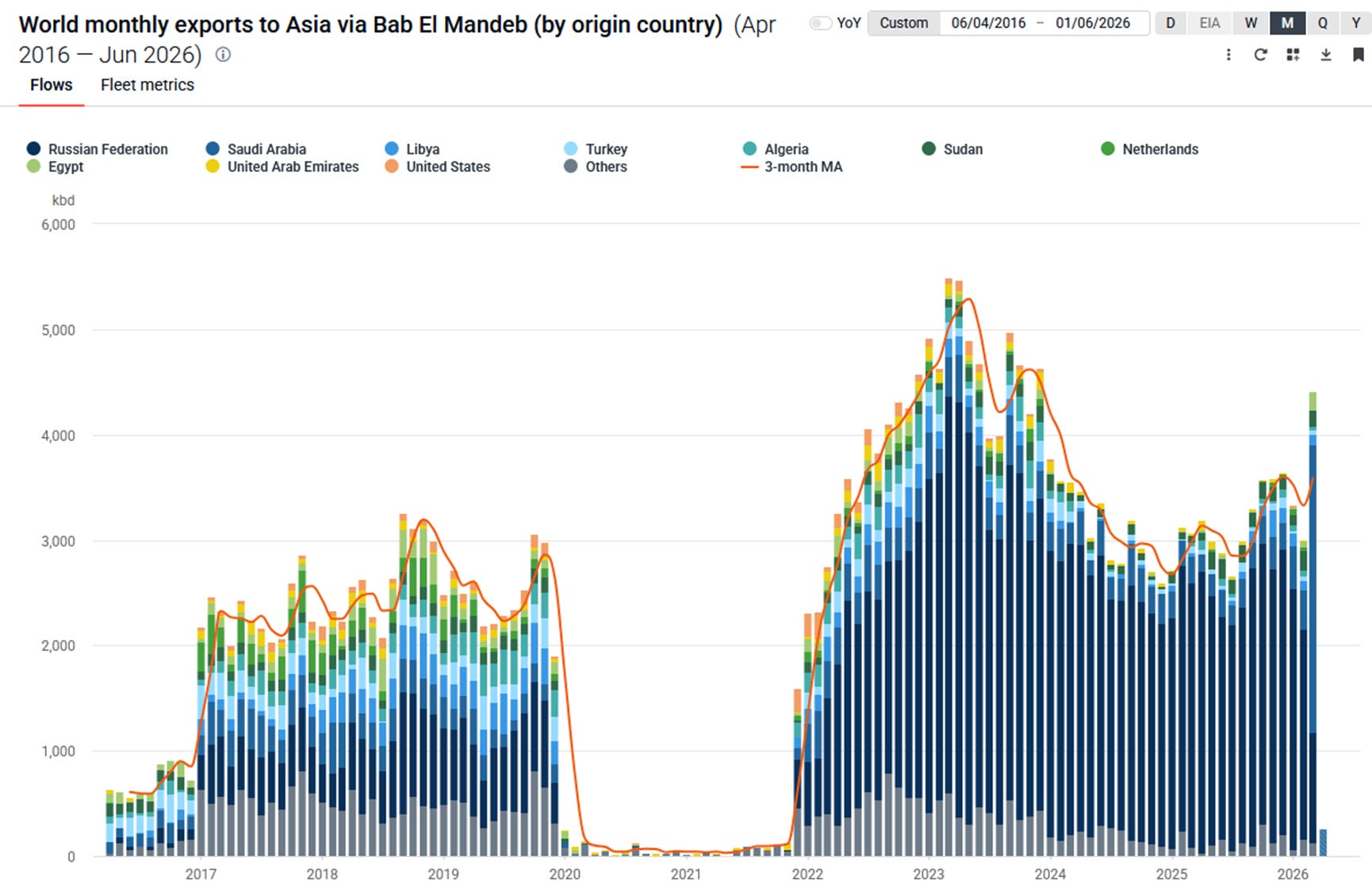

Iran’s attempts to charge tolls, restrict passage, or impose conditions are violations of this framework. The Houthis applied a similar blackmail playbook, with fewer means, in the Bab el-Mandeb, which was functionally closed between 2019 and 2021. None of this required sea mines or heavy lifting. A credible threat, perhaps a drone strike, is sufficient.

Back then, a U.S.-Saudi coalition restored order. U.N. conventions are only as strong as the power that enforces them, which is why Pax Americana enabled freeriding, with significant net benefits accruing to the United States and its reserve currency, while Britain and France carried a large share of the burden without the exorbitant privilege of the global reserve currency.

Regardless, what if no one feels responsible in the current situation? Iran is a state actor behaving like a terrorist organisation, a different calibre altogether than the Houthi militias. It is all rather problematic in an age of “butter”, not “guns”, and misguided strongman leadership.

If that insight takes hold, why would Turkey not begin charging additional fees for “security services” at the Bosporus, beyond the limited service fees already in place, a point correctly highlighted by Andrey Sizov, a Black Sea agri-commodity expert? It is vastly more capable than Iran.

China is an order of magnitude more capable than Iran and Turkey combined, and could deploy a far more sophisticated version of the same economic leverage in the Taiwan Strait, with severe short-term consequences for global semiconductor supply chains and corresponding retaliation, perhaps in the Strait of Malacca, Gibraltar or the Panama Canal.

It serves no one’s long-term interest. Yet history has periods in which old lessons must be re-learned before reason prevails. As Henry Kissinger noted in one of his final interviews with the Financial Times on 20 July 2018:

“Trump may be one of those figures in history who appears from time to time to mark the end of an era and to force it to give up its old pretences. It doesn’t necessarily mean that he knows this, or that he is considering any great alternative. It could just be an accident.”

The Fog of War Collides with the Midterms

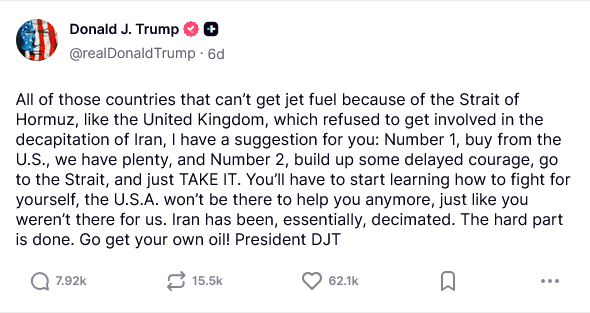

Meanwhile, Trump’s increasingly erratic and aggressive reactions suggest his administration was not prepared for this. He certainly did not prepare his voter base for a war of attrition to regain control of Hormuz, the true weapon of mass destruction in the wrong hands. That leaves this, in the eyes of his electorate, as a war of choice. But is it? Regaining control of Hormuz does not look optional.

The problem is perception. United States voters, and others, are not yet ready to see this clearly. A few weeks of higher oil prices and three cancelled flights in Timbuktu will not suffice. A prolonged recession would.

Iran’s regime has not acted irrationally in the past, but it does not follow standard cost-benefit logic. Its decisions are shaped by ideology and regime survival under stress. Historically, it has behaved risk-averse in gains and risk-seeking in losses, particularly during the Iran-Iraq war. Under pressure, concessions are framed as losses, not gains. That makes escalation more likely as stress increases. Trump’s approach, and his reliance on deadlines, is therefore counterproductive.

Trump appeared to be aiming for an evolutionary version of Operation Midnight Hammer in Iran and Absolute Resolve in Venezuela, a compressed playbook of surgical air strikes, special operations and real-time intelligence integration. A campaign to prevent a nuclear Iran, reassert control over Middle Eastern oil flows and engineer regime change, with a Nobel Peace Prize as the epilogue. Peace through strength. The fog of war denied him that sequence.

Earlier military success reinforced a false sense of control. Operation Absolute Resolve, months in planning and executed in hours, likely shaped expectations of repeatability. That misread carried into Iran.

The administration failed to explain the stakes of this war, and its necessity, to the electorate. On the contrary, Trump campaigned on avoiding Middle Eastern entanglements. For his base, and for a majority of Americans, this remains a war of choice.

How is the war going? If one were to ask the President whether he would start this war again with the knowledge he has today, the answer would undoubtedly be no, in a classified setting. In public, this war remains a roaring success. Despite undisputed battlefield success, including air dominance, the honest assessment is that the President lost control of this war weeks ago.

Trump is left with two bad choices. (A) He can walk away and leave unfinished business, with immeasurable risk to American soft power and the petrodollar system. Or (B) he can attempt to finish the job while fighting a political war at home, which makes a military resolution increasingly unattainable the longer the conflict drags on, as the fog of war collides with the midterms.

The regime in Iran understands this. In its own calculus, time has become an ally. And in this conflict, perception dictates reality.

Some argue this conflict has no military solution. I am less certain of that, but I am certain an air campaign alone will not suffice. As historian Stephen Kotkin notes, regimes can fail at almost everything as long as they retain a monopoly on violence against its own people.

This regime appears to have fine-tuned, and at the same time decentralised and automated, its response functions when faced with internal uprisings or external attacks, brutally so. But who is going to take the Kalashnikovs out of their hands? It is not the F-35 pilot from Israel or the United States.

At the same time, regimes have a habit of looking invincible the day before they collapse. These apparent contradictions often coexist, as seen in the fall of the Berlin Wall and the subsequent breakdown of the Soviet Union.

Overlay this with the current negotiation dynamic. Deadlines, threats and tactical escalation are now part of the playbook. By the time this is read, positions will have shifted again, whether through escalation, delay or partial retreat.

What matters is the pattern. TACO and short-term escalation are not mutually exclusive. They tend to occur together, as both sides seek to improve their bargaining position before stepping back. Iran understands this well.

Likewise, the President may still get lucky on the battlefield, but from where I sit the most likely outcome is that the United States and Israel win the battles, yet lose the war and the peace that follows, at least in the near term and until the regime eventually collapses. That leaves a highly uncertain set-up for the global economy in 2026 and likely into 2027.

Who Controls the Barrels?

My Base Case is TACO this month, followed by a series of bilateral “arrangements” between Iran and producing countries such as Iraq, Kuwait and Bahrain. India and other emerging Asian economies are likely to pursue similar deals. That will not be sufficient to avoid a global recession, and several of these dynamics will overlap.

I do not expect Saudi Arabia or the UAE to negotiate. They think in generations, not in midterms. Their barrels return fully, either through a clean reopening, via physical bypass pipelines or under coalition force. There is no middle ground.

Likewise, China, Japan, South Korea and Europe are unlikely to enter bilateral agreements with institutional weight, as doing so would set a dangerous legal precedent for global maritime commerce.

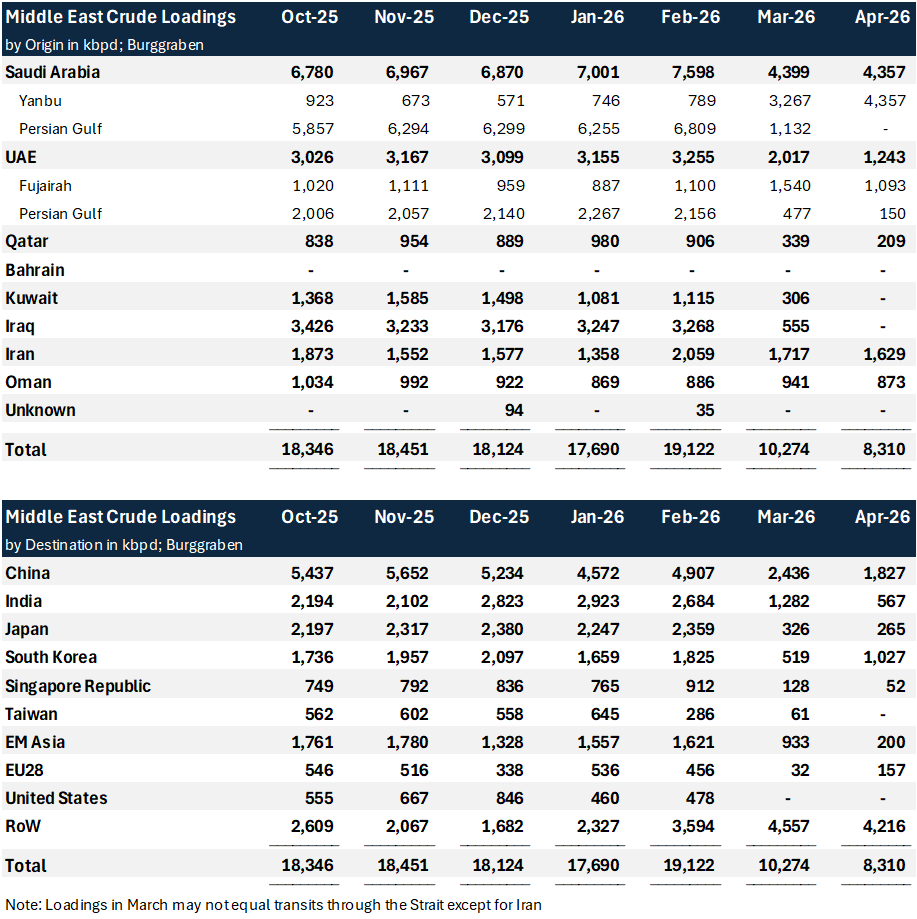

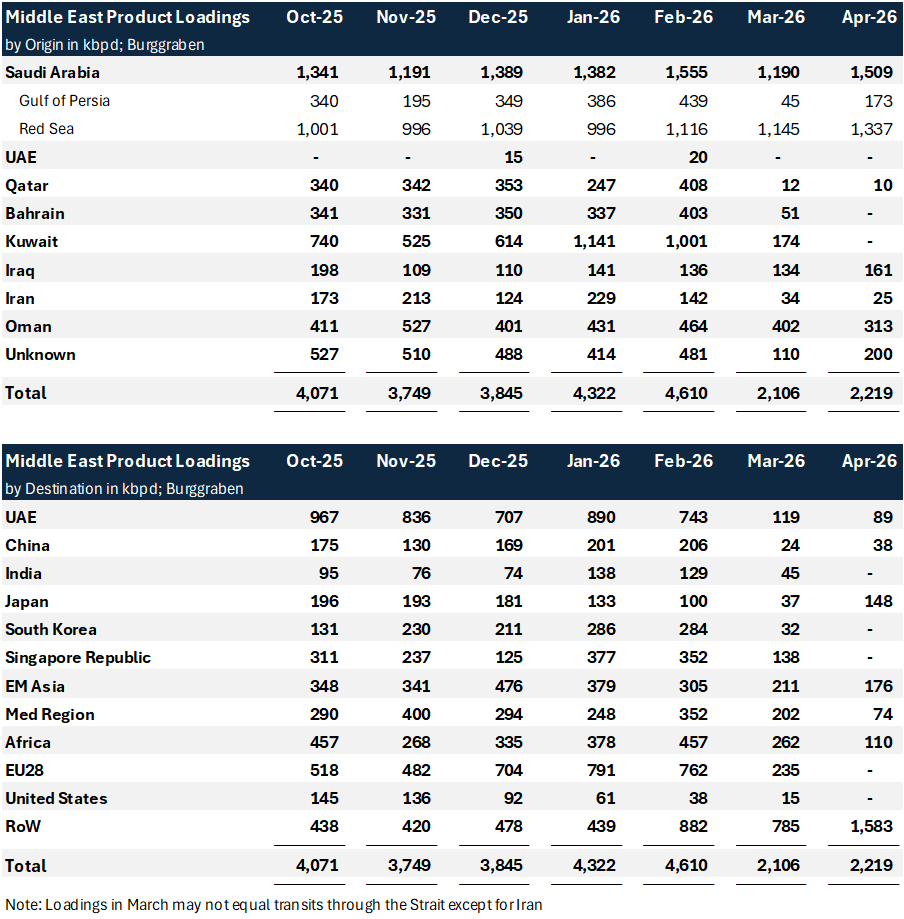

The tables below illustrate crude oil import flows by origin and help frame regional exposure. Japan sources roughly 90%+ of its refinery intake from the Middle East, South Korea and Taiwan are similarly exposed, while China sits closer to 50%. These are material dependencies, but they are only one part of the equation.

Inventories, strategic reserves, crude quality and refinery configurations matter just as much, if not more, in determining how this shock propagates. Take China. It holds the world’s largest crude oil and product inventories. That provides time, not immunity.

The CCP can afford to watch its geopolitical rival, the United States, absorb not just the economic strain, but also the geopolitical damage to its soft power and, ultimately, to the petrodollar system, for an extended period at current run rates before it needs to react. As Napoleon once put it, do not interrupt your enemy when he is making a mistake. And it will not.

An important caveat here. The stakes for the global economy are so high that a pronounced recession could alter this calculus and force “creative” solutions, such as a Two-Tier Transit System with an Oman and Iran lane in the Strait of Hormuz. But without the United States interrupting Iranian barrel flows as well, I see no reason why Tehran would concede to such an arrangement. Nor is it clear what that would imply for transit frequency. Let us call this the “Face Saving Case”.

The Upside Case assumes a negotiated settlement between the United States and Iran, restoring most transits within 3–24 months, the time required to repair war damage and bring shut-in fields back. The track record for such agreements is poor, particularly with regimes in the Middle East, Russia or North Korea.

The Downside Case extends the disruption to the Bab el-Mandeb, adding a second chokepoint and a further layer of escalation. More short-term pain may be required to avoid longer-term damage. Such an escalation would frontload the economic impact by several months, removing an additional 2–3mbpd from the market (some barrels will continue exiting at the Suez Canal).

Both TACO and the Downside Case may ultimately require a coalition of the willing, boots on the ground and naval escorts to restore flows to perhaps 75%. Alternatively, new pipeline infrastructure could restore capacity over a 3–5 year horizon. The most likely outcome is a combination of these paths, as no single solution satisfies all parties.

What matters is timing. Even if the regime proves more fragile than it appears, that does not resolve the current disruption. The sequencing runs the other way. First, the hot phase of the conflict ends. Only then do internal dynamics begin to matter.

No one takes to the streets to be hit by “friendly fire”. From there, several outcomes are possible, including a more democratic one. But for oil markets and global trade, that sits firmly in the second order.

Barrel Counting: Houston, We Have a Problem

Given my domain in commodities, and energy in particular, I have more confidence in what this means for barrel counting. And I have nothing but bad news. The damage to the physical oil market has already been done for prices to return to pre-war levels in 2026, while the risk of significant economic downside increases by the day.

The oil market, and with it the global economy, cannot function with 10–15% less energy supply, from oil to gas to fertiliser to helium. Physical commodities must balance. We cannot consume what we do not supply on any given day.

That sounds trivial, but the implication is not. Global supply chains, in energy and beyond, were never designed to absorb a shock of this magnitude. We do not hold strategic reserves for everything, everywhere, for 3–5 months while policymakers search for solutions. Meanwhile, so-called OPEC spare capacity of 4–6mbpd is trapped within the conflict zone too.

That leaves one mechanism to restore balance: demand destruction. Prices must rise until consumption falls by 10–15%. Every country will feel this, directly or indirectly, and the adjustment is already underway.

My table above shows the scale of the disruption in a 102mbpd global liquids market, pre-war. If the Base Case extends into July, the world effectively draws down crude inventories by 30%. For context, a 1–3% change in inventories is sufficient to move prices materially.

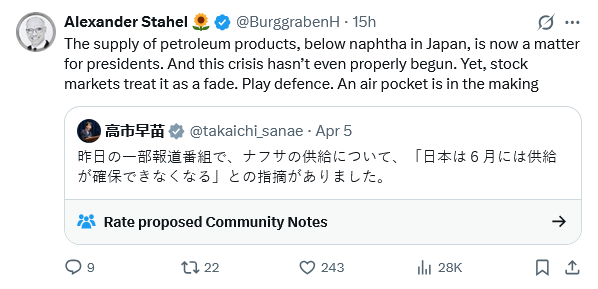

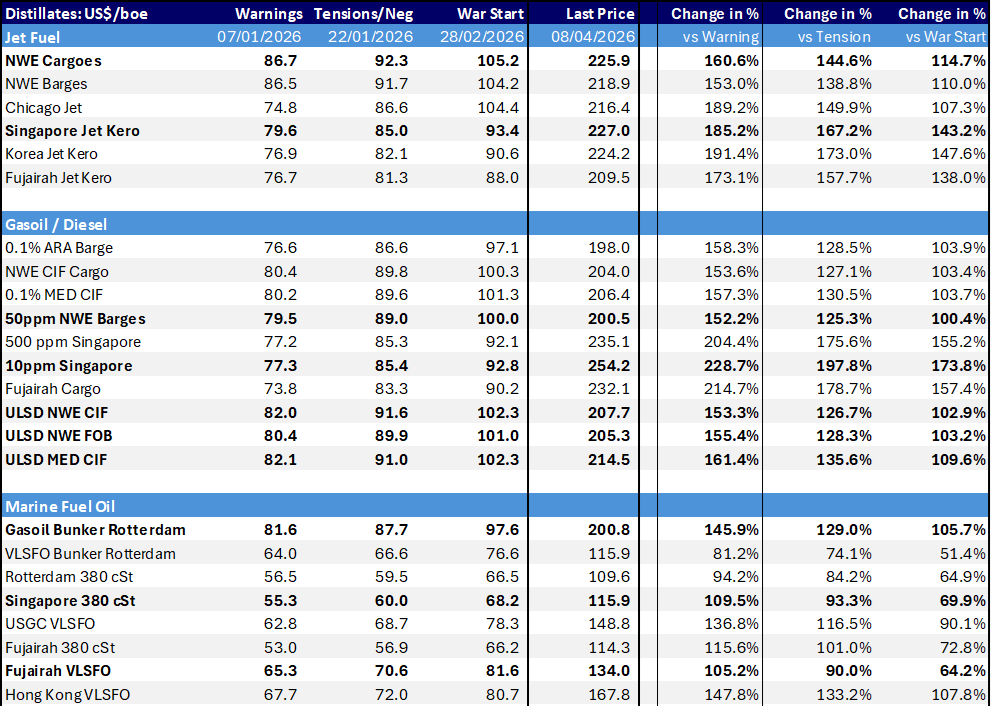

And inventories are the least of the problem. Over the same period, petroleum products begin to run short in unexpected places. Jet fuel, diesel and naphtha shortages in Asia become ground zero of the crisis.

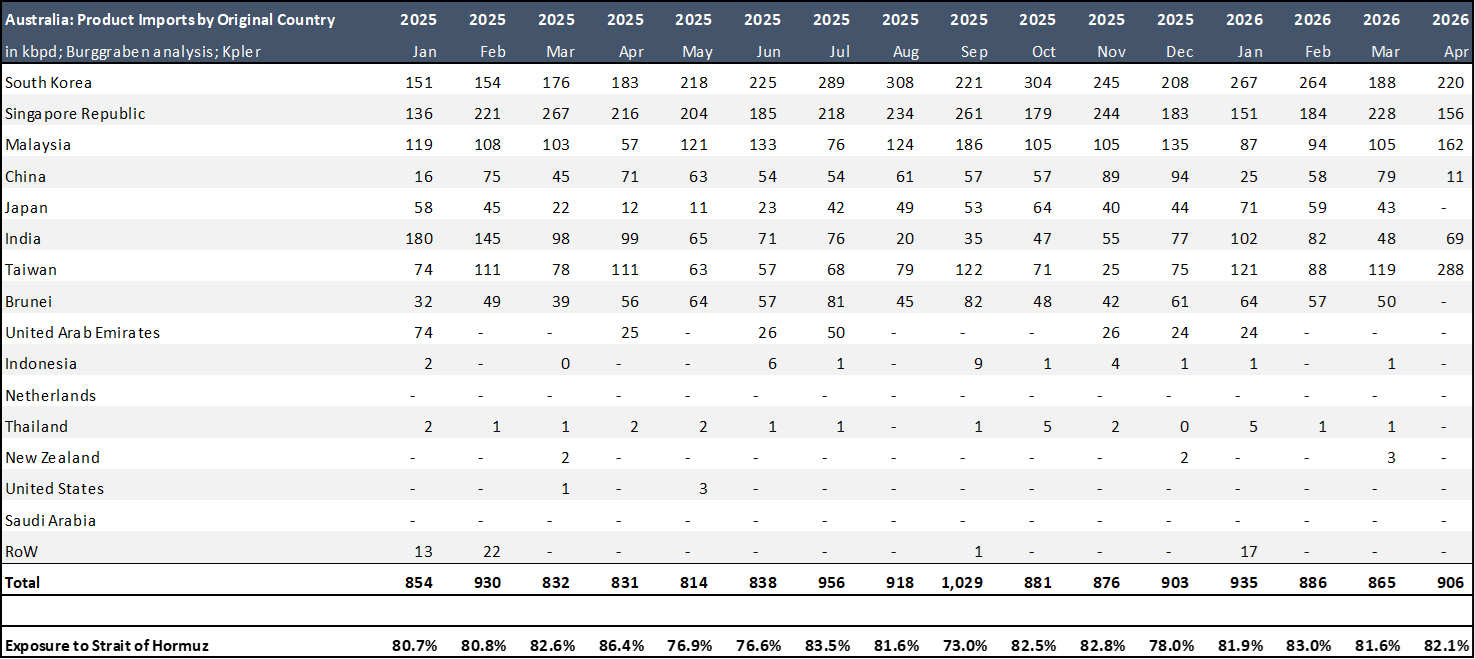

Japan illustrates the constraint and as mentioned above. It imports 92% of its refinery intake from the Middle East. These heavy-sour barrels are not easily replaced, and substitution materially alters product yields. Replace Arab Medium with WTI Midland and diesel output falls sharply, potentially by 30%, given refinery configurations. Crude quality matters in this crisis. I will explain why in a future episode in detail.

The situation is not much easier for South Korea, Singapore, China or Australia. Australia, in particular, has shut domestic refining capacity and now imports 90% of its 1.1mbpd product demand from regional hubs. The vulnerability is obvious.

Pro-tip: avoid Asia as a travel destination while the Strait remains functionally closed.

But this is not just an Asian problem. Europe, Africa and the Americas will feel it, if only through higher prices at the pump. The disruption transmits through supply chains. Today’s naphtha shortage in Japan becomes tomorrow’s feedstock constraint in Germany.

So when European or Asian policymakers argue that this is not “their” war, the instinct is understandable. But I am afraid the supply chain won’t care who started it. It will only reflect who pays for it.

Covid-Type Demand Destruction

The required level of demand destruction to rebalance the oil market can be measured, and it implies a prolonged and difficult global recession. Think of it this way: to remove 10–15mbpd of demand, slightly less with temporary SPR releases, we require sustained periods of US$200+ oil.

When I say oil, I mean the entire barrel, gasoline, diesel, jet fuel, naphtha, marine fuels and more. In reality, we are already there for key products. Diesel and jet fuel prices are trading well above US$200 per barrel in many regions. The invisible hand is already at work.

Demand does not adjust in a straight line, nor evenly across regions or products. Product prices determine elasticity. Destruction takes time, not only because consumers react with a lag, but because price signals transmit from products back to crude with delay.

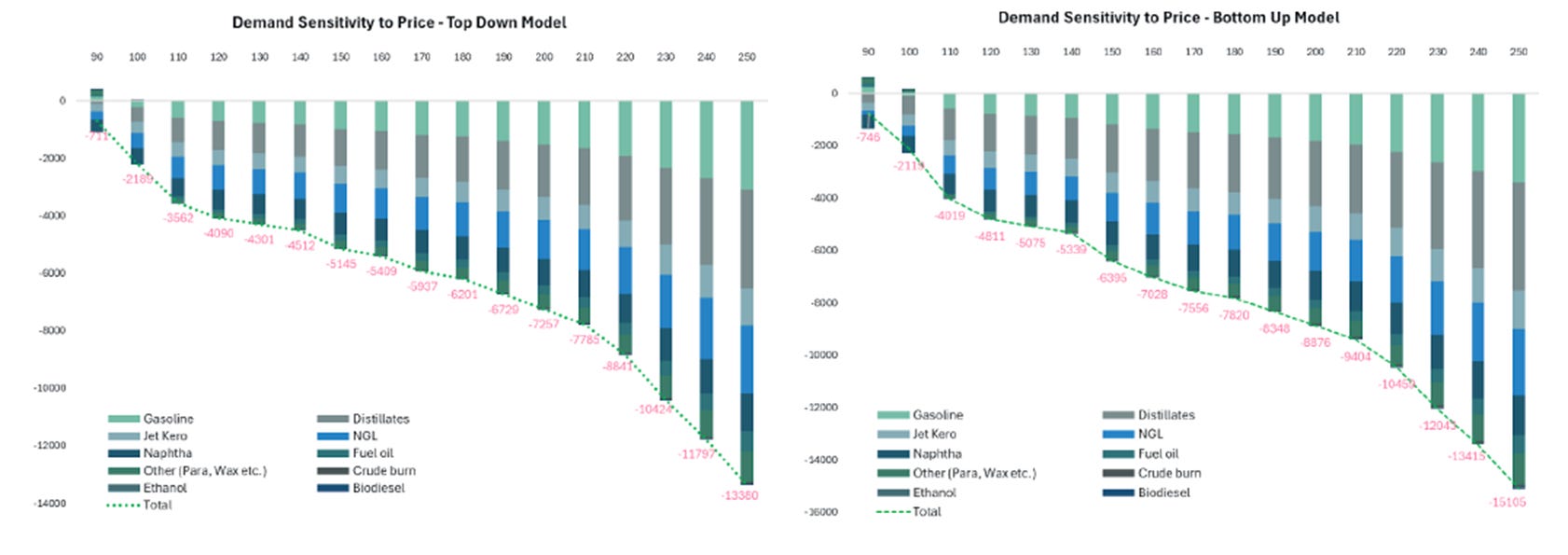

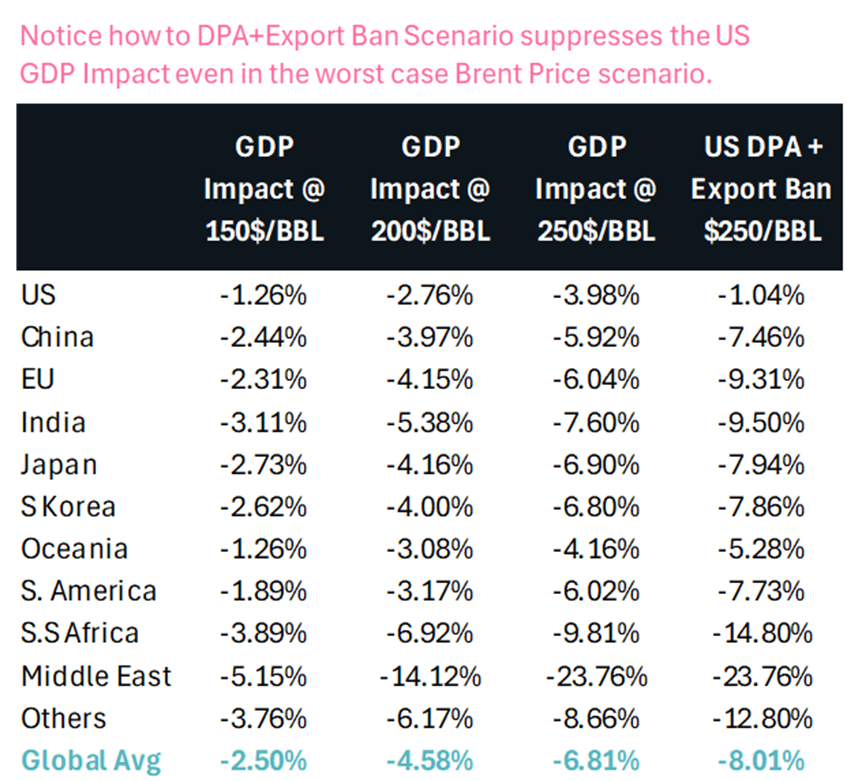

In the scenario below, Lakshmi Sreekumar at Capital One, one of the most rigorous oil analysts in the field, models demand response to sustained price levels over a 90-day period. Her work draws on five decades of demand elasticity studies.

Once the scale and timing of demand destruction are understood, the broader economic consequences follow. This is not a marginal adjustment. It is a global shock. If realised, it would rank among the most economically stressful periods in modern history, arguably more insidious than Covid.

During Covid, central banks operated in a deflationary environment. They could supply liquidity aggressively without immediate inflation constraints, even if they ultimately overdid it on the fiscal side. This time is different.

This scenario places us squarely in a stagflationary environment in the near term, followed by a sharp recession as demand destruction restores balance. Central banks are constrained. Cutting rates into inflation is not viable, and balance sheet expansion carries credibility risks. Markets will anticipate the downturn well in advance.

Lakshmi’s framework highlights key convexity thresholds at US$150, US$200 and US$250 per barrel. At each level, different parts of the global economy begin to shut down. The burden is not evenly distributed. While oil intensity has declined in developed economies, it remains high across emerging markets, where the adjustment will be more severe.

Think of it as Covid without policy mandates. Instead of governments forcing people to stay home, the market does. Daily life simply becomes unaffordable in pockets of the global economy.

Misalignment of Incentives

In summary, this situation is too complex, with too many actors, constraints and conflicting incentives, to resolve cleanly through negotiation alone. Meanwhile, the oil system still has to balance physically and cannot wait for diplomacy and reason to play out.

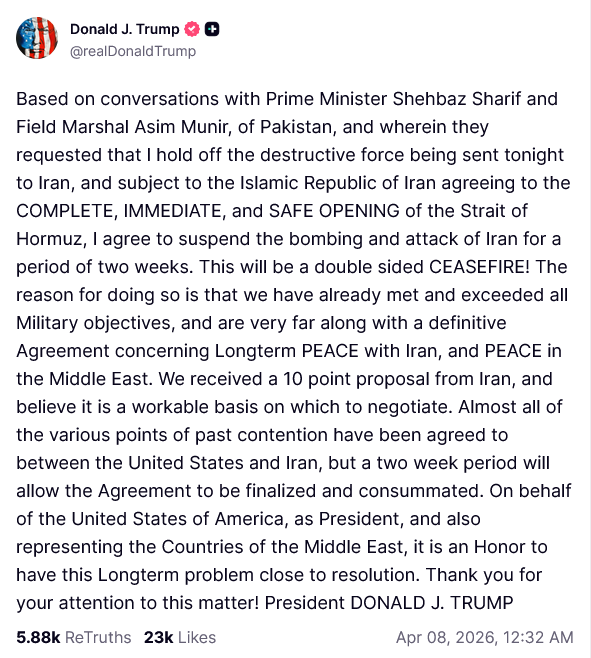

The core issue is misalignment at the top. The key actor, the United States, is under political pressure to end the war quickly. That leaves the door open for a partial outcome, TACO without a full reopening of the Strait. The two are not the same. A ceasefire does not guarantee restored transits. Disruptions can persist for months, possibly years, and until bypasses are fully established.

As I am writing this, the latest development underscores the point. President Trump has agreed to suspend bombing for two weeks, conditional on Iran agreeing to the “complete, immediate and safe opening” of the Strait. This is not resolution. It is negotiation through escalation.

Deadlines, threats and tactical retreats follow the same pattern. Escalate to gain leverage, step back to test the response, then reset expectations. TACO and short-term escalation are not contradictions. They are part of the same process.

Crucially, a temporary ceasefire does not equate to a reopening of the Strait. The suspension of force is conditional, fragile and reversible. Markets trade flows, not press releases.

Nor are bilateral solutions straightforward. As outlined earlier, Saudi Arabia and the UAE will not negotiate with Iran under coercion. On the demand side, OECD countries and China have no incentive to legitimise any restriction on freedom of navigation. At least I cannot see how the EU Commission will sign a toll service arrangement with this Iranian regime. But I keep an open mind, I promise.

Some countries, including Japan, South Korea and parts of Southern Europe, may be forced to muddle through via an Oman lane. But that solution is operationally uncertain and slow to establish. Parts of EM Asia may well cut “deals” with Iran, but that will not rebalance the global market and would set a dangerous precedent few can afford.

Even regime change, often cited as a release valve, does not solve the near-term problem. It is highly unlikely to occur on a timeline that restores flows within weeks, even if it happens in 2026.

A global recession is therefore the most likely mechanism through which a durable solution emerges, whether through restored flows in Hormuz or a broader geopolitical reset. Before that, alignment among participants remains unlikely.

Closing Thoughts

This Substack will lay out the case in detail across multiple episodes, with a data-driven approach that prioritises precision over narrative comfort.

The executive summary remains free. Subsequent coverage will return behind the paywall. The next instalments will go deeper, at times technical, covering critical aspects of the oil market such as crude quality and why it matters in this context.

As an independent investor based in Switzerland, I have the freedom to call it as I see it. Oil sits firmly within my circle of competence, and I feel obliged to prepare those willing to listen for what lies ahead. And warn people of foolish statements like the below.

There seems to be a persistent narrative that losing 5–6% of global oil supply is manageable. Firstly, it will be much more. Second, it isn’t for many people around the world. It is a category error to say otherwise.

Oil is not priced on total supply. It is priced at the margin.

The world does not price oil at 100mbpd supply versus 94mbpd. It prices the last barrel that clears the market. Remove that barrel, and you are not “6% short”. You are short the barrel that sets the price.

Think of it as musical chairs. One hundred people, one hundred chairs. Everything works. Remove five chairs. The price of the remaining chairs does not rise by 5%. It goes vertical, because five people get nothing.

That is how energy markets behave. They are tight systems with very limited buffers.

This is why comparisons to prior “surplus” narratives miss the point. Yes, the market may have been heading for a 1-3mbpd surplus in 2026. That surplus no longer exists. More importantly, what matters is not the average balance, but the available flexibility at the margin and crude quality feeds around the global refinery system, among many other things.

Spare capacity is limited, geographically constrained and, in this case, trapped within the conflict zone. What looks like a 5–6% disruption on paper can represent a far larger share of the system’s usable flexibility. That is when prices move non-linearly, as already evident in distillates, with a broad move above US$200 for diesel and jet fuel globally, not just in isolated pockets.

Demand does not adjust smoothly either. It is stepwise. Airlines do not fly 70% of a route. Consumers do not partially commute. Industrial plants do not run at arbitrary utilisation rates. They run, until they stop. Listen to the fisherman in France from two days ago.

This is why prices must rise sharply to force actual demand destruction. And why that adjustment is both abrupt and economically painful. Commodity markets are not set by averages. They are set by the barrel that does not exist.

Anyway, this will become an extensive coverage because this is an unusually complex crisis. It deserves more than headlines and hot takes. I hope you all agree. Stay safe out there.

Warm regards,

Alexander Stahel

Excellent Note - Thanks

I've followed your stuff for a few years, as a non paying subscriber and your (generally bearish) commentary was more accurate than my hopium.

This one pushed me over the paywall as the markets think all is magically fixed